Bankruptcy of the Cathedralmodel

- Content -

---

|

In the early '30s the residual debt of the Roaring Twenties totaled more than 250% of GDP. Today, the still-growing debt of the Dollar Standard Era reaches more than 350%. At all other times - that is over the plains and valleys of the rest of the century, debt to GDP averaged only about 150%. -- The Daily Reckoning, February 6, 2004 |

|

"In the last five years the U.S. economy has added over $15 trillion in debt bringing total outstanding debt to $37 trillion..." -- Storm Watch, July 16, 2004 |

---

America: the world's biggest hedge fund

|

1990: $5 trillion - 2006: More than $2,000 trillion Gross World Production 2006: $47 trillion Bankrupt? |

---

---

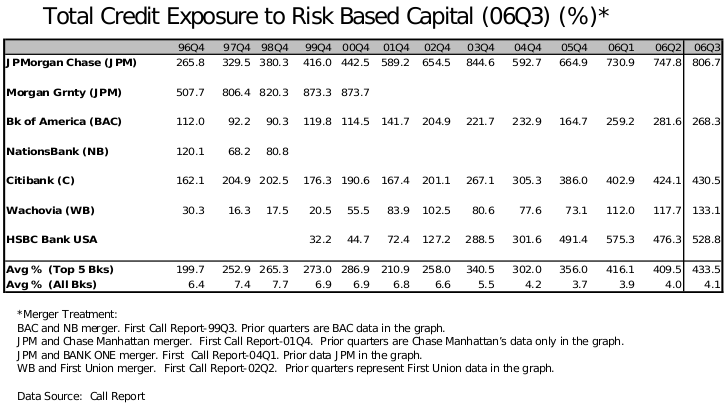

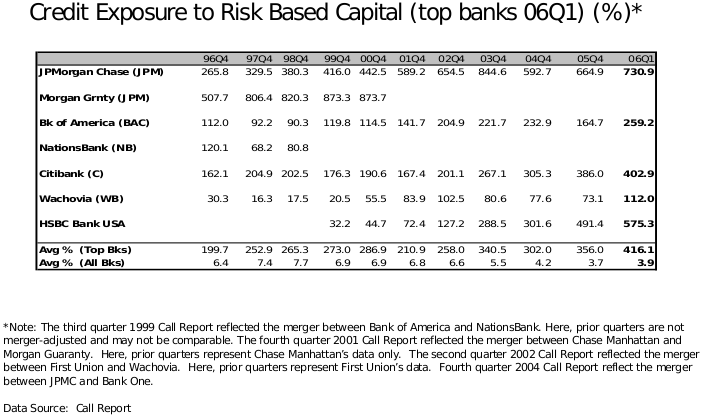

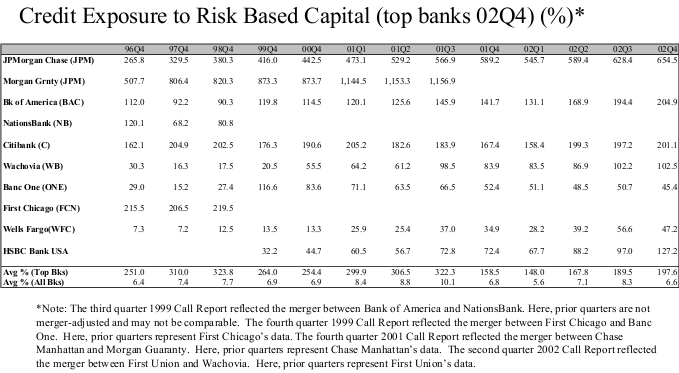

Interest Rate Increases Stress US Banking

---

( M3 Growth: Dollar Zone (Shadow Government Statistics - M3b) / Euro Zone )

|

First-Half Global Liquidity Watch "To be sure, the CDO market is the tip of a derivatives iceberg when it comes to risk obfuscation and market pricing issues. Arcane instruments, lack of transparency, and tainted markets can (and did) remain non-issues for quite some time. Yet the longer the period of chicanery the more abruptly greed will inevitably succumb to fear. Today, markets are turning fearful. They are fearful of the quality of assets supporting the massive securitization marketplace. They are fearful of mispricing. They are fearful of liquidity. And, importantly, they are fearful of the ramifications of - in today's overheated financial environment - any meaningful movement away from risk assets. All the fears are justified."

|

|

This Time It's Different (Or Is it?) (pdf) "A particularly common story concerns structured notes. How many banks bought such notes through bond salesmen with the idea that they carried high returns but were safe because they were backed by the Federal Home Loan Bank System and the federal government? One banker even told us he didn't have to worry about his securities because his broker "controlled" the risk for him. In many cases, bankers never gave a second thought to the significant risks structured notes presented to their banks."

|

|

"...the lending is increasingly being orchestrated from outside the regulated banking industry, by hedge funds and other credit investors that are often supervised only indirectly, if at all. These are especially big in the booming market for credit derivatives, which are also traded outside public exchanges."

|

|

"Timothy Geithner, president and chief executive officer of the New York Federal Reserve Bank, warned in a speech ("Risk Management Challenges in the US Financial System") before the Global Association of Risk Professionals' (GARP) seventh annual Risk Management Convention and Exhibition in New York City on February 28 that the scale of the over-the-counter (OTC) derivatives markets is dangerously large."

|

|

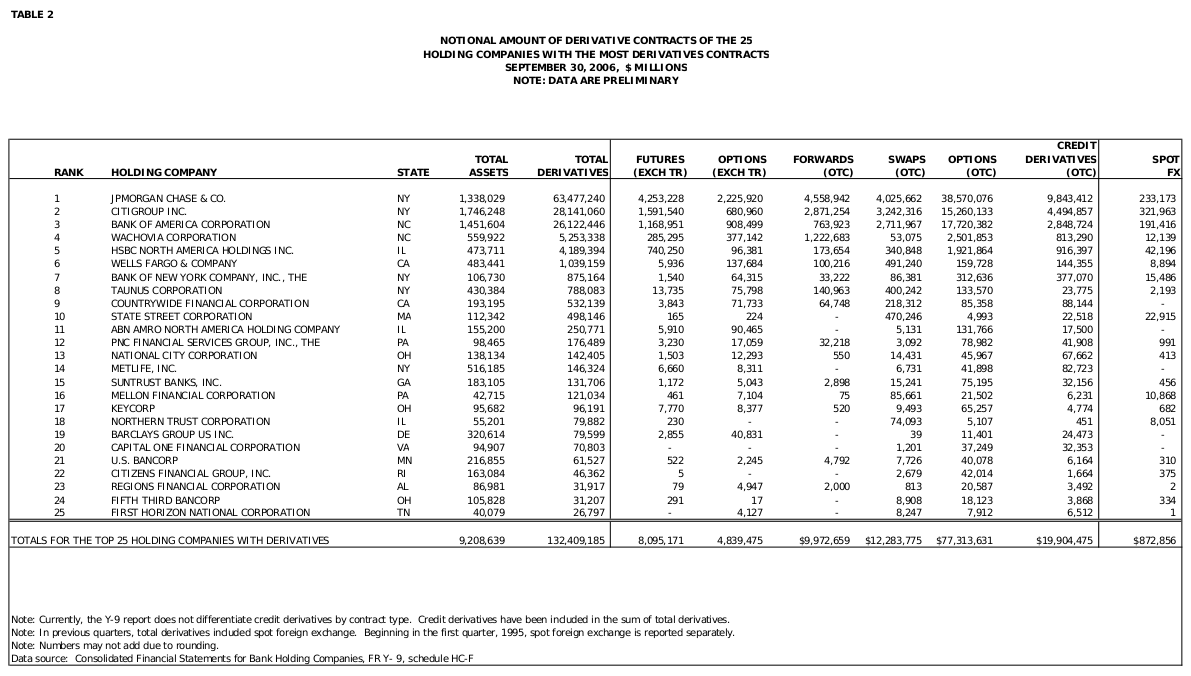

The dream machine: invention of credit derivatives "By 1997, Demchak and Masters came up with their Big Idea: a product known as Bistro, short for Broad Index Secured Trust Offering. (Bankers who work in the world of derivatives love creating odd names out of complex acronyms - it appeals to their problem-solving skills, no doubt.) What Bistro did was to use credit derivatives to "clean up" a bank's balance sheet. The scheme started by taking a basket of bank loans and separating out - in accounting terms - the theoretical risk that these loans would turn sour from the loans themselves. This default risk was usually then sold to a "paper" company, known as a special purpose vehicle, which then issued bonds that investors could buy. If lots of loans went into default, the value of these bonds would fall, of course; but if the loans were honoured, the bonds would be a safe bet for the investors. Either way, the point was this: anyone buying such bonds was essentially betting on the risk of loan default. And as long as the deal was structured in a way that made the bonds look cheap, relative to the risk of default, then investors would think they had got a good deal. The pricing itself was based on what had happened to banks' loan books in recent years (together with some complex number crunching). The deal looked even better for the original bank. For the act of selling the default risk on to new investors had crucial regulatory implications. International banking rules say that banks have to hold a certain level of spare funds (or reserves) to protect themselves from the danger that their loans might turn bad. However, since the banks had sold the risk of default on to somebody else, they could now argue that they did not need to hold these funds. To anybody outside the world of finance, this might look odd (after all, the banks were still making loans); but the regulators accepted this argument, since the risk had moved, in accounting terms. And that let the banks free up funds to make even more loans. It was the financial equivalent of calorie-free chocolate: almost too good to be true. Hancock's group started using Bistro to clean up JPMorgan's own portfolio of loans. Then they started offering it to other banks. And within the space of a few months, they were handling not just billions of dollars of loans, but tens of billions, and then hundreds of billions. It was an intoxicating time for the young bankers. Many had been impoverished graduates just a few years earlier; now they were earning bonuses bigger than most had ever dared to imagine. Not that they had any time to spend the cash: as demand swelled, JPMorgan's tiny team - which still numbered just a few dozen - found themselves almost every waking hour in each others' company. "The business we were doing grew exponentially," recalls Duhon. "We went out and 'Bistro-ed' everything we could.""

|

|

'Tougher' rules in credit derivatives market? "Fourteen credit derivative dealers met with the New York Federal Reserve Bank on Thursday and vowed to police the booming market themselves to keep regulators from doing it, a meeting participant said."

|

| Global liquidity - Saturated - "Central banks were supposedly the guardians of money. Yet, they have created the biggest liquidity bubble in history."

|

| Fed Governor warns of "mega-banks" "The creation of mega-banks also heightens concerns about systemic risk. When banking activities are concentrated in a few very large banking companies, shocks to these individual companies could have repercussions to the financial system and the real economy." -- Simon Kwan (June 17, 2004) |

| Banks... really learned nothing? "The present situation “is not dissimilar” to the one that preceded the collapse of LTCM, says Michael Thompson, a strategist at RiskMetrics, a consultancy that specialises in the very risk-management models that banks use. Like LTCM, banks are building up huge positions in the expectation that markets will remain stable. They are, says Mr Thompson, “walking themselves to the edge of the cliff”. This is because—as all past financial crises have shown—the risk-management models they use woefully underestimate the savage effects of big shocks, when everybody is trying to wriggle out of their positions at the same time..." -- Buttonwood (February 17, 2004) |

| "They are yesterday’s heroes. Central banks ruled the world during some 22 years of disinflation. But like most champions, they have overstayed their welcome. The world’s major central banks — the Federal Reserve, the Bank of Japan, and the European Central Bank — have squandered the capital they built up in the long and arduous war against inflation. And now, with their policy arsenals dangerously depleted, they are woefully ill-equipped to cope with the ever-daunting complexities of a post-inflation era. Bondholders beware: Your once-proud defenders have met their match. I fear modern-day central banking is on the brink of systemic failure." -- Stephen Roach (Morgan Stanley February 17, 2004) |

| What Does Mr. Greenspan Really Think? “Another way to look at this, especially the issue of financial collapse, is to consider some of the things that don’t make it into the press. For example, the Bank for International Settlements (the “BIS”), which is the central bank for all central banks, recently formed something called the Financial Stability Institute. They didn’t form that Financial Stability Institute because everything is okay. They have a problem.

|

|

Capitalism's bad apples: It's the barrel that's rotten "...Yet Skilling was quite effective in laying the blame for the financial mess at the door of unregulated structured finance (derivatives), which Congress, under pressure from the finance industry, had repeatedly refused to regulate, albeit also at the urging of the both the Federal Reserve Board and the Treasury, and even the SEC, which only faintly warned against accounting manipulation of corporate balance sheets. It is ironic that the head of a company [Enron] that had vigorously championed deregulation and market discipline, a company whose spectacular recent growth was financed by wholesale theft from the future if not directly the public, by booking future revenue [Mark-to-Market] as current income, deferring associated liabilities as off-balance-sheet future capital expenditure, by disguising loans as income with hedges in derivative transactions that produce spectacular instant profit, is now calling for Congress to regulate the widespread use of the "material adverse change" clause in derivative contracts and related financing that allows investors to pull their funds abruptly and completely on practically no notice." -- Henry C K Liu (Aug 1, 2002) |

| Derivative hedge funds are ticking like time bombs "In a visit to my office in June of last year, the chairman of a major gold producer was asked his perspective on the risks that rising gold prices might have to the financial system. "Just how large do you think the train wreck will be when the rest of this industry decides to close out its hedge book" was the question posed. He answered that he thought it could even bring down a major Wall Street investment bank. Indeed, as we learned from the terrifying crumble of John Meriwether's ill-fated Long Term Capital hedge fund, the American banking system can be compromised by the unraveling of derivatives of a single hedge fund. It's not hard to imagine how the fall of an industrial labyrinth on the scale of Minos' that is the gold industry might take out at least one major American bank." -- Prescott Crocker (March 25, 2002) |

|

"The leitmotif is "innovation", and many respectables are extremely worried. I argued in Counterpunch earlier (June 15 and July 26) that gloom prevailed among experts responsible for overseeing national and global financial affairs, especially the Bank for International Settlements, but I grossly underestimated the extent of anxieties among those who know the most about these matters. "

More important, over the past months officials at much higher levels have also become much more articulate and concerned about the dominant trends in global finance and the fact that risks are quickly growing and are now enormous. Generally, people who think of themselves as leftists know precious little of those questions, questions that are vital to the very health of the status quo. But those most au courant with global financial trends have been sounding the alarm louder and louder. The problem is that capitalism has become more aberrant, improvised, and self-destructive than ever. It is the age of the predator and gamblers, people who want to get very rich very quickly and are wholly oblivious to the larger consequences. Power exists but the theory to describe the economy that was inherited from the 19th century bears no relationship whatsoever to the way it operates in practice, a fact more and more recognized by those who favor a system of privilege and inequality. Even some senior officials at the International Monetary Fund (IMF) now acknowledge that the theory that powerful organizations cherish is based on outmoded 19th-century illusions. "Reconstructing economic theory virtually from scratch" and purging economics of "neoclassical idiocies", or that its "demonstrably false conceptual core is sustained by inertia alone", is now the subject of very acute articles in none other than the Financial Times, the most influential and widely read daily in the capitalist world."

|

|

Economists have a blind spot for finance "The economics profession, as a whole, has a blind spot for finance. Economists conduct their analyses without reference to the creation of credit and debt. They regard money as "neutral" and ignore, on the whole, the role of credit. As Schumpeter once wrote, economists treat the "phenomena of economic life ...in terms of goods and services, of decisions about them, and of relations between them. Money enters the picture only in the modest role of a technical device that has been adopted in order to facilitate transactions." So the Bank of England's model of the UK has no debt components. Of course it is recognised that there are, every so often, monetary "disorders" - but money is "of secondary importance in the explanation of the economic process of reality."

This explains economic orthodoxy's blind spot and apathy towards the creation of today's gigantic credit/debt bubble - a bubble that should cause greater concern than the rampant housing bubbles of Anglo-American economies. It also explains the poor record and extraordinary optimism of economic analysts and forecasters. In a survey in March 2001, 95% of US economic forecasters predicted that there would not be a recession in 2001. "Too bad", notes Nouriel Roubini, "that the recession had already started exactly in March of that year."

|

|

Global Resilience: At What Cost? "The excesses of the global liquidity cycle explain much of the new cushioning role world financial markets have played in warding off major shocks during the past several years. While we see visible manifestations of excess liquidity everywhere -- asset bubbles, historically low spreads on risky assets, and unusually low volatility in major equity and bond markets -- we are lacking in good metrics to measure it. For a forecaster, that makes it tough to render a judgment as to when -- and under what conditions -- the liquidity cycle goes from being a tailwind to a headwind insofar as its impacts on world financial markets and the global economy are concerned. The explosive growth of non-traditional sources of liquidity -- especially derivatives -- seriously complicates the measurement problem. BIS data put the notional value of global over-the-counter derivatives markets at US$285 trillion in December 2005 -- up more than 40% from volumes just two years earlier and more than six times the nominal level of world GDP. The notion of being awash in liquidity takes on a very different meaning in this context."

|

|

Derivatives regulation must be 'borderless' "Three of the world's most powerful financial regulators have taken the unusual step of issuing a joint warning that individual nations cannot contain some of the risks posed by the explosive growth of derivatives and must collaborate across borders."

|

|

"What would happen if there was another LTCM today? --- The Connecticut-based institutional service Bridgewater Daily Observations, which itself manages over $150 billion, has been asking this disturbing question and getting a fairly disturbing answer..."

|

|

The (US) housing bubble has popped "To me, it's not debatable that the real-estate bust is starting to gather steam. The top was approximately when Time Magazine published its June 12, 2005, cover story: "Home $weet Home: Why We're Going Gaga Over Real Estate".."

|

|

Europe simulates financial meltdown "However, the report warned that hedge funds and credit derivatives were sources of concern "as related risks remain opaque and they have become extremely relevant in assessing financial stability both across borders and across all financial sectors"."

|

| After the fall (World Housing Bubble) "This boom is unprecedented in terms of both the number of countries involved and the record size of house-price gains. Measured by the increase in asset values over the past five years, the global housing boom is the biggest financial bubble in history (see article). The bigger the boom, the bigger the eventual bust."

|

|

The Global Systemic Crisis and the End of `Free Trade' "This is just a typical indication of what I mean by $400 trillion in derivatives obligations. We have a category of finances, which is not real, but which has a very real effect on the economy. Imagine a gambling casino, and you've got somebody putting a few dollars on the table in the gambling casino—gambling against somebody else, at the crap table. But, standing behind these gamblers, are bettors, who are betting on what the outcome of the gamblers' betting will be—they're called side-bets. You have the guy who bets on the horse; you have the guy who bets on the bettor on the horse—side-bets. What these financial derivatives are, are essentially side-bets, gambling side-bets. There is no actual value involved in them. There's no trade. There's no item in there, where something is sold; it's simply an arbitrary financial transaction, a gambling debt. But these gambling debts have taken over the world system. These gambling debts are much larger—$400 trillion, which is what this is approaching, or has already exceeded—is much larger than the entire world economy combined. These gambling debts are now controlling the world financial system." -- Lyndon LaRouche (2002) |

|

The Crisis of Global Capitalism: Open Society Endangered "As the system (Market Capitalism) expands, the economic function comes to dominate the lives of people and society. It penetrates into areas that were previously not considered economic, such as culture, politics and the professions. The centre is the provider of capital, the periphery is the user of capital. The rules of the game are skewed in favour of the centre." (p.104). "...people weighted down by a concern for others are liable to do less well than these who are free of all moral scruples. In this way, social values undergo what may be described as a process of adverse natural selection: the unscrupulous come on the top. This is one of the most disturbing aspect of the global capitalist system. " (p.199). "A transactional society undermines social values and loosens moral constrains. Social values express concern for others. They imply that an individual belongs to a community, be it family, a tribe, a nation or humankind, whose interests must have precedence over individual's self-interest. But transactional market economy is anything but a community. Everybody must look out for his or her own interests and moral scruples can become an encumbrance in a dog-eat-dog world. " (p. 75). -- George Soros (1997) |

|

High Noon: 20 Global Problems - 20 Years to Solve Them "Worldwide rules on minimum risk capital for banks are in a state of flux. An older "capital ratio" formula has now been phased out by a committee managed by the Bank for International Settlements (BIS) and is about to be replaced by a new setup that takes hundreds of pages to describe-raising quite a few contrivers. "(p. 123). "Accounting rules for financial institutions remain oddly unclear in some major respects. One reason banking sectors are so opaque and able to hide serious problems for so long is that loans remain booked at their historical value… At any rate, much work remains to be done on the accounting underpinnings of sound banking. "(p. 123). "Hedge funds remain poorly known and monitored financial creatures. The Long-Term Capital Management debacle in late 1998 (Chapter 7) brought hedge funds into the public limelight, and they have never left is since. Hedge funds are private funds that borrow up to fifteen to thirty times their own resources and then further leverage up to gigantic position through futures, options and other derivatives-tools enabling sophisticated bets on the prices or price differences of other assets. Long-Term Capital Management, with equity capital of less than $5 billion, had times more than $1trillion in derivatives exposure. These hedge funds are mostly in the business of chasing tiny pricing aberrations between pairs of financial assets, which they then exploit at the large scale made possible by their large leverage. But sometimes their positions are more like huge outright bets on the possible rise of fall of a financial asset's price. In 1997, one hedge fund held positions on the Thai baht amounting to 20 percent of the Thai central bank's reserves. An intriguing recent casualty was the U.S. energy company Enron, with turned out to have a large hedge fund operation inside its belly when it collapsed in December 2001. Worldwide, there are now 6,000 to 7,000 hedge funds controlling assets worth $500 billion, not including less visible ones like the Enron case. There is some work going on to develop some principles for stronger monitoring by governments of hedge funds and their potentially destabilising activities, but it's still early days. "(p 123, 124). -- Jean-François Rischard (2002) |

| "Derivatives played an unprecedented key role in the Asian financial crisis of 1997, alongside the growth of fund flows to Asian NIEs [newly industrialized economies], as part of financial globalization in unregulated global foreign exchange, capital and debt markets. Derivatives facilitate the growth in private fund flows by unbundling the risks associated with financial vehicles, such as bank loans, stocks, bonds and direct physical investment, and reallocating the risks more efficiently by expanding the distribution and the level of aggregate risk. They also facilitate efforts by many financial entities to raise their risk-to-capital ratios to dodge regulatory safeguards, manipulate accounting rules and evade taxation. Foreign exchange forwards and swaps are used to hedge against floating exchange rates as well as to speculate on fixed exchange rate vulnerability, while total return swaps (TRS) are used to capture "carry trade" profit from interest rate differential between pegged currencies." "...Derivatives trading in over-the-counter (OTC) markets were, and still are, neither registered nor systematically reported to the market. Thus the full risk exposure in the system is not known until the crisis hits. In macroeconomic terms, derivatives have the structural effect of privatizing the incremental efficiency (profits) while socializing the risk (losses) associated with such profits. This is done by extracting value through rising risk/return ratios by siphoning off part of the incremental return to known private parties while passing on the full incremental risk to faceless third parties spread throughout the system. Since the spread was minuscule, profit incentive pushed for massive increases in volume." -- Henry C K Liu (2002) |

| “Derivatives generate reported earnings that

are often wildly overstated and based on estimates whose inaccuracy

may not be exposed for many years" -- Warren Buffett (2003) |

| Parmalat was of course meddling with derivatives too… under auspices of the banks… "It may also be worth looking at the role of the banks, many of which were happy to earn money by arranging Parmalat's derivatives transactions, without regard to the longer-term consequences." -- BBC Q&A: Parmalat's troubles |

| "In no circumstances enter the derivatives trading market without first agreeing it in writing with me ... at some time in the future it could bring the world's financial system to its knees." -- Sir Julian Hodge Gambling on Derivatives |

{kind=link}