Credit Crunch – The New Diet Snack for Financial Markets - By Satyajit Das

Posted by ProjectC

"The fall in asset prices has “wealth” effects. US consumption, based on borrowing against the inflated values of financial assets, drives the export driven economies of Asia, Eastern Europe and Latin America. Lower commodity prices already point to slower global growth. While main street was trying the assess the fallout, Wall Street was already issuing “pink slips” by the thousands as banks and mortgage lenders shed staff.

...

Understanding and valuing structured securities requires a higher degree in a quantitative discipline, a super computer and a vivid imagination.

...

Diffusion of risk across the globe to unregulated investors subject to variable financial disclosure rule is inconsistent with transparency. Investors like hedge funds have steadfastly fought for increasing transparency and disclosure, except when it relates to their own activities. One central banker observed that in the good old days, there would have been no problem as the risk would be where it always was - at the banks.

...

John Kenneth Galbraith observed that: “in central banking as in diplomacy, style, conservative tailoring, and an easy association with the affluent count greatly and results far much less.” Central bankers fueled the liquidity factories through excessive monetary growth and low interest rates. They championed financial innovation and “new age” finance theories. The risks of a diffuse, globally interlinked, highly leveraged financial system were ignored.

...

Crash diets rarely work. The solution requires will power, a sensible but reduced food intake and exercise. In financial markets, the resolution requires regulatory will and an imposition of market disciplines on errant investors and banks. It also requires a sharp reduction in debt levels and addressing the problems of risk transfer, model risk and market transparency."

Credit Crunch – The New Diet Snack for Financial Markets

By Satyajit Das

September 5, 2007

Source

Satyajit Das works in the area of financial derivatives and risk management. He is the author of a number of key reference works on derivatives and risk management and is the author of Traders, Guns & Money: Knowns and Unknowns in the Dazzling World of Derivatives (2006, FT-Prentice Hall).

Living in the Kaliyuga …

Inflexion points in financial markets are difficult to identify. As Yogi Berra observed: “making predictions is difficult, especially about the future”.

In Indian mythology, we are in the Age of Kali - the last age. The world ends when Kali dances the dance of death. There are no such clear markers in markets. Recently, we came close - Jim Cramer, a CNBC pundit, launched a “we’re in Armageddon” tirade on air. Embattled Bear Stearns’ CFO Samuel Molinaro pleaded: “I’ve been out here for 22 years, and this is as bad as I’ve seen it in the fixed-income markets.” Kali had begun to shake her booty. The credit bubble was finally deflating.

In 2007, householders in “cabbage-ville USA” (an English fund manager’s term) failed to make repayments triggering a global credit crisis. Markets ruminated about “a re-pricing of risk”. The faux “business as usual” calm masked the fact that the problems threaten to be the single largest credit crisis since the Savings and Loans collapse in the USA in the 1980s.

The early 2000s were a period of “too much” and “too little” – too much liquidity, too much leverage, too much complex financial engineering, too little return for risk, too little understanding of the risks. Steven Rattner (from hedge fund Quadrangle Group) summed it up in the pages of the Wall Street Journal: “No exaggeration is required to pronounce unequivocally that money is available today in quantities, at prices and on terms never before seen in the 100-plus years since U.S. financial markets reached full flower.” Traditional money fueled by loose monetary policy, excessive capital flows and now turbo-charged by “financial engineering” lies at the heart of the current credit crisis.

Structured Credit - Supersize My Debt!

Candyfloss (cotton candy or fairy floss) - spun sugar - consists mostly of air. It is the quintessential experience of a visit to a fairground. New financial technology is “candy floss” money 1- money spun out and expanded into ever larger servings. Derivatives, securitisation and collateralised lending allow fundamental changes in credit markets and leverage.

Derivatives – highly leveraged commercial bets on movements in prices of interest rates, currencies, shares and commodities - can be used to manage or create risk. Investors increasingly use derivatives to increase risk to earn higher returns. As at the end of 2006, derivative outstandings were around $485 trillion. In comparison, total global Gross Domestic Product is around $ 60 trillion. Derivative trading created additional liquidity and leverage.

Derivatives on credit instruments are a relatively recent innovation. A credit default swap (“CDS”) is credit insurance on a specific company. The buyer of protection (usually a bank who has lent money to the company) pays the seller of protection (usually an investor) a fee. In return, the seller of protection covers the bank buying protection against losses should the company go bankrupt. CDOs are steroid-fueled mortgage loan securitisations. A portfolio of loans, bonds or mortgages is assembled. Interest and principal from the underlying portfolio is used to make payments on the CDO securities issued to investors.

In a CDS contract, unlike a loan or bond, the investor is not required to pay the full face value. CDS volumes are not limited to the outstanding amount of debt. General Motors has around US$130 billion of debt. CDS volumes on GM are around 6 to 10 times that. CDSs allowed the credit markets to “supersize” trading volumes.

In CDOs, the bank uses the dexterity of the Iron Chef to cut and dice the risk of the underlying loans. “Tranching” allows the creation of different CDO securities - equity, mezzanine and senior debt. Equity receives high returns and bears the most risk. If there are losses on the portfolio of loans then equity takes the first losses. The senior note holders take the least risk as they are first in line to get paid and last to lose. They get low returns but more than on comparable traditional securities. Mezzanine (code for subordinated debt) is somewhere in between. Tranching is used to alter credit ratings on portfolios of A/ BBB loans to manufacture AAA/ AA securities.

CDOs concentrate risk and increase the potential gain or loss for a given event. CDOs are based on “diversified” underlying portfolios; e.g. a $1,000 million portfolio made up of 100 loans of $10 million each. Assume that if any of the 100 firms goes bankrupt, you lose $6 million (60% of $10 million). If the equity tranche is $20 million (2%), then the investor takes the risk of the first 3 firms to go bankrupt out of the 100 firms in the portfolio ($20 million of losses divided by $ 6 million). The investor’s risk is not diversified; it is taking the risk on the 3 worst firms out of the 100 in the portfolio.

If the investor invested $20 million in the 100 loans ($200,000 per corporation calculated as $20 million divided by 100), then 3 defaults in the portfolio would result in a loss of only $0.36 million (loss of $120,000 per company (60% of $200,000) times 3). In a CDO, if there are the same 3 losses then the equity investor losses $20 million. The leverage to default is 56 times ($20 million versus $0.36 million). Frequently, the holder of the equity tranche borrows to fund its stake further increasing leverage. A regulated bank can leverage around 12 ½ times. CDOs concentrate credit risk – the term is “toxic waste”.

The structured credit market has supersized debt levels using techniques of staggering complexity, incomprehensible to all but a small group of practitioners. The market was so “like hot” that one professional confessed that even his headhunter had been recruited into a structured credit role at an investment bank.

Would you like debt with that?

Repurchase agreements or “repos” (secured lending against government securities) and margin loans (lending secured against stocks) are well established. Now, investors use repos to raise substantial amounts against any security or instrument, including distressed debt.

Investors routinely structure asset purchases as a total return swap (“TRS”). The investor receives the return on the asset (income and increases in price) in return for paying the cost of holding the asset (decreases in price and the funding cost of the dealer). The investor posts a modest initial margin or “haircut” and promises to post more cash if the value of the asset declines. The trader has bought the asset with money borrowed from the dealer with which it entered into the TRS. Favorable regulatory rules, optimistic views of liquidity (the collateral must be sold if the borrower fails to pay) and faith in the models used to set the margins drives aggressive use of collateral increasing available liquidity and leverage.

Banks have also institutionalized the collateral game in a plethora of off-balance sheet structures – arbitrage or conduit vehicles; structured investment vehicles (“SIVs”). The vehicles purchase high quality securities like AAA or AA rated CDOs and fund them with short-term borrowings (usually, commercial paper (“CP”) issued to money market funds). $1.2 trillion or 53% of the $2.2 trillion commercial paper in the US market is now asset backed, around 50% by mortgages. When investors now buy assets, the dealers automatically ask: “would you like debt with that?”

The New Liquidity Factory 2

Banks traditionally wrote and funded their loans. In the new money game, banks “originate” loans, “warehouse” them on their balance sheet for a short time and then “distribute” them to investors using CDOs. Banks require less capital, as they don’t hold the loan for its full term. The process encouraged declines in credit standards. The game relies on the ongoing liquidity of the market for securitised debt.

When the loans are sold, the bank effectively receives the difference between the interest on the loan and the return demanded by the investor “upfront”. As loans are sold off, more loans must be written. Ever larger volumes are necessary to maintain profitability forcing banks to rely on brokers. In the new money game, banks increased loan volumes, reduced capital available to absorb risk and lowered the credit quality of their loans all at the same time.

Insurance companies, pension funds, asset managers, banks, and private clients are buyers of credit risk. Hedge funds moved into the credit markets in search of higher returns based on leveraged structured credit instruments. The high returns came with additional risks – a lack of liquidity and complexity of the securities. Buyers from Switzerland to Slovakia, Boston to Beijing bought up credit risk. A feature of credit investing was that the complexity and risk of structures was inversely related to the understanding of the investor being sold it.

In the new liquidity factory, investors did the borrowing - hedge funds borrowed against investments; traders borrowed cheap money (especially yen at zero interest rates) to fund high yielding assets in the famous carry trade. Financial engineering disguised leverage so that an investor’s balance sheet today does not tell you the amount of leverage being employed.

The new liquidity factory is self-perpetuating. If you bought assets with borrowings then as the asset went up in price you borrowed more money against it. In an accelerating spiral, asset prices rise as debt fuels demand for the asset. Higher prices decrease the returns forcing the investors to borrow more to increase returns. Bankers became adept at stripping money out of existing assets that had appreciated in price, such as homes. In the USA, UK and Australia – the fast debt nations - home equity borrowing funded a frantic debt addiction.

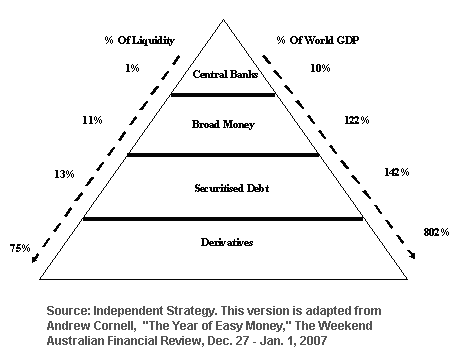

By the early 2000s, the new liquidity factory had created a money pyramid that had no parallel in history. Diagram 1 sets out the money pile in modern markets. The tsunami of debt fueled price increases in financial assets - debt, equity, property, infrastructure. The current market volatility is not simply a correction in prices but this gigantic liquidity bubble unwinding.

Diagram 1 - The New Liquidity Factory

Lying NINJA Mortgagors

A German banker recently accosted me: “vhat does a poor American defaulting in Looneyville, West Virginia have to do vith me?” There were also defaults in Gravity Iowa, Mars Pennsylvania, Paris Texas, Venus Texas, Earth Texas, and Saturn Texas.

Deregulation, abundant liquidity and rising house prices encouraged lenders to target less affluent borrowers with poor credit histories who have long been excluded from the American dream of home ownership. Sub-prime and Alt A housing loans included “innovations." 3

Loan to value ratio (“LVR”) – traditional mortgages provide 70-80% of appraised value. Sub-prime mortgages had more aggressive LVRs including “negative” equity loans (the lender is lending more than the value of the house). Undisclosed “piggyback” loans and silent second mortgages eliminated any deposit requirement.

· Interest payments – sub-prime mortgage repayments sometimes don’t cover interest on the loan. In a negative amortisation loan, the principal actually increases as interest is not covered. There were “teaser’ rates – 2/ 28 mortgages where there are artificially low rates (as low as 1%) for the first 2 years with the loan interest being reset at the end of the “honeymoon” period. Sub-prime mortgages were adjustable rate mortgages (“ARMs”) rather than the more typically fixed rate mortgages.

· Jumbo loans – these were large loans (above $417,000) needed to finance more expensive houses.

· Credit review and loan underwriting standards – the mortgage industry increasingly relied on credit scoring models. Statements of income and assets are not checked. Outsourcing mortgage origination to brokers and shifting of risk to investors led to a systematic decline in underwriting standards.

· Purpose of loan –a high portion of sub-prime was directed to monetisation of the equity in existing homes; between 2000 and 2005, total mortgage equity withdrawal increased from $289 billion to $900 billion.

Around 2003/ 2004, the housing market began to slow. Banks and brokers maintained volumes at the expense of even weaker standards. LVRs rose and documentation requirements collapsed. Demand for long term high-yielding assets from investors fueled the securitisation process that the sub-prime market relied upon. By 2007, the sub-prime market accounted for 20% of new mortgages and 10% of all mortgage debt.

Francois Rabelias, the French author, observed in the 16th Century: “debts and lies are generally mixed together.” NINJAs (“no income, no jobs or assets”) able to sign their name could buy a house without any money. In 2006, Casey Serin, a 24-year old web designer from Sacramento, bought seven houses in five months with US$2.2 million in debt. He lied about his income on “no document” loans. He had no deposit. In 2007, three of his houses were repossessed. The others face foreclosure. Serin’s website - www.Iamfacingforeclosure.com - has become the symbol of the excesses of the sub-prime mortgage market. 4

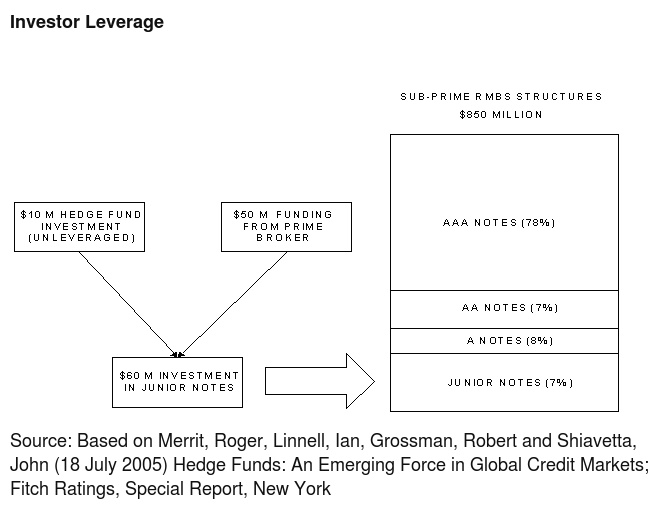

Hedge funds used leverage to “enhance” returns on sub-prime debt. Diagram 2 shows how a hedge fund uses $10 million to take the risk of the first $60 million of losses on a $850 million portfolio.5

Diagram 2

A Gradual and Sudden Death

The “Goldilocks” economy led one commentator in 1997 to assume that the business cycle had been abolished.

“We are watching the beginning of a global economic boom on a scale never experienced before. We have entered a period of sustained growth that could double the world’s economy every dozen years and bring increasing prosperity for – quite literally – billions of people on the planet. We are riding the early waves of a 25-year run of a greatly expanding economy that will do much to solve seemingly intractable problems like poverty and to ease tensions throughout the world. And we’ll do it without blowing the lid of the environment.”6

Unfortunately, interest rates increased sharply in the US. Central banks tightened liquidity as inflation rose driven by higher oil prices, increasing costs in emerging countries and infrastructure constraints. US house prices stalled and then fell. Delinquencies in sub-prime mortgages reached 15% and in some types of loans approached 30%. Defaults rose. at an uncomfortable 45’ gradient.

In 2006, an asset based securities credit index had been introduced to provide some transparency to the opaque CDO and mortgage markets. The ABX.HE (Asset backed Securities Home Equity) entailed five separate indexes (AAA, AA, A, BBB, BBB-) referencing similarly rated tranches of 20 securitisation transactions. The BBB- 2006 index collapsed from around 100 to initially 60-70% of face value to its current level of around 30-40%. It was, according to Luiz Inácio Lula da Silva (“Lula”), President of Brazil, “an eminently American crisis” caused by people trying to make a lot of “third-class money”.

Like engine oil, credit lubricates and keeps the financial motor running. The oil was leaking out rapidly; the engine was seizing up. Sub-prime mortgage lenders closed as business dried up. Investments in the riskier tranches of the securitised mortgage pools were worthless. Investors in the “safe”, higher rated – AAA and AA tranches – had real problems In a typical securitisation, actual losses on the underlying mortgages pool would need to rise above 15-30% before they suffered losses. AAA tranches were quoted (if you could find a quote!) at between 80-90% of face value. AA and A were lower again.

The AAA rating of senior tranches is based on layers of subordinated securities to absorb initial losses. As expected losses mounted and the lower layers were eaten away, the AAA rating of the senior tranche fell leading to mark-to-market losses – i.e. what the security is worth if sold today.

If the investor ignored the current (mark-to-market) value then the investor was still unlikely to actually lose money. Lower ratings forced investors to sell as the securities did not comply with investment guidelines triggering losses. Hedge funds who borrowed against the securities faced margin calls as the values fell. The lenders tightened lending conditions reducing leverage and increasing the cost. “No man’s credit was now as good as his money”. 7

The sub-prime problem was initially a “specific problem” and “contained”. It was neither. It spread quickly and efficiently – the word “contagion” appeared. By August 2007, credit markets had just about ceased to function. A veteran commentator – Ian Kerr - compared the current credit crunch to death from radiation – CDOs, particularly those with sub-prime exposure, now stood for Chernobyl Death Obligations!

Bear in the Woods

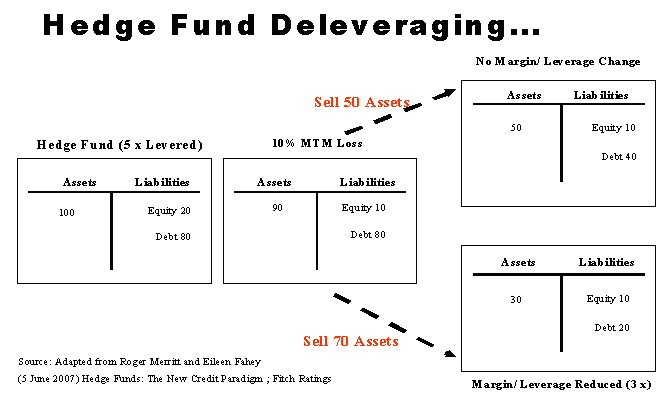

Two investors see a bear in the woods. One investor starts to run. “You can’t outrun a bear,” the other investor shouts. “I can outrun you!” responds the running investor. Investors and financial institutions now wanted to get their money out before the cash vanished. Diagram 3 sets out how selling is exaggerated in a highly leveraged world.

Diagram 3

The United States absorbs around 85% of total global capital flows, or over $500 billion each year. Asia and Europe were the world’s largest net suppliers of capital, followed by Russia and the Middle East. Cross border debt flows funded the US government debt (up $400 billion) and a rapid expansion in US private debt (up $1.3 trillion). A key growth area was asset-backed securities (“ABS”), including mortgage-backed securities (“MBS”), reflecting the strong US housing market and high levels of home-equity lending.8 Global money funded the US debt binge and now global investors suffered losses.

Exposure started to show up in unlikely places via asset backed CP – money market funds. One institution disclosed that CDOs and subprime mortgages were classified as “cash and short term” on its balance sheet. Structured funding vehicles were unable to issue ABS backed CP. They drew on standby funding arrangements. Banks refused to fund arguing material changes in circumstances. Others had to forage down the back of the sofa for any loose change to add to their dwindling liquidity.

Reduced leverage and higher costs of funding affected hedge funds. Quantitative funds suffered large losses as forced selling and a liquidity driven market caused models to fail. Hedge fund investors, concerned about declines in returns and sharp falls in value, lodged redemption requests forcing selling. Goldman Sachs was forced to step in to offer liquidity support to one of its funds.

Overheated equity markets fell despite strong corporate earnings and a growing economy on concerns about less abundant and higher priced debt. Stock values exaggerated by the possibility of debt fuelled private equity bids fell sharply. Financial stocks fell as the losses, bailout costs and loss of future earnings was factored in. Investors regretted not taking Will Rogers advice: “don't gamble; take all your savings and buy some good stock and hold it till it goes up, then sell it. If it don’t go up, don’t buy it.”

Market credit spreads and margins rose sharply. There was a flight to quality – government securities and cash. Liquidity vaporized as fear about counterparty default meant that normal transactions between financial institutions became difficult. Risk lending dried up. AAA rated non sub-prime mortgage-backed securities could not be placed.

There is no difference between a run on a bank and shutdown of access to funding from the capital markets. US mortgage lenders faced old-fashioned runs. Central banks pumped money into the system. The Fed cut the discount rate. Four major US banks used the discount window: “to encourage its use by other financial institutions”. They did not need cash. It was a sign of strength. In the words of financial historian, Charles Geisst, it was : “like someone from the Upper East Side being seen in .. Wal-Mart”.

The problem was credit risk not liquidity. Lack of information and diffusion of risk meant that no one was certain who had exposure to what or to whom. EBC governor Jean-Claude Trichet pleaded for everybody “to keep their composure”. It was reminiscent of Emperor Hirohito’s response to the bombing of Hiroshima: “the War situation has developed not necessarily to Japan’s advantage.”

Waiting for the Shoe to Fall…

A pyroclastic flow is a part of volcanic eruptions consisting of lethal currents of Tephra (hot 1000 degrees Celsius gas, ash and rock) travelling at up to 700 km/hour. Pompeii was famously engulfed by pyroclastic flows in AD 79. The sub-prime losses had morphed into a fully-fledged “credit crunch”, the pyroclastic flow of financial markets.

Hedge funds faced substantial redemption requests especially from funds-of-funds in charge of allocating hot money in the coming months. Interest rates on large volumes of sub-prime mortgages were due to increase (by 3-4%) in 2008. The impact on delinquencies and losses were unknown.

The same model as sub-prime is used for leveraged funding in private equity, infrastructure and property financing. Banks underwrote the loans, warehoused them and then repackaged and distributed them to investors in the form of CDOs. Deterioration in credit standards was evident. “Covenant lite” loans where the borrower did not agree to normal financial restrictions had become fashionable. “Toggle” loans where borrowers could pay in cash interest using new debt (Pay-In-Kind or PIK securities) abounded.

The same model as sub-prime is used, worryingly, for funding highly leveraged private equity, infrastructure and property transactions. As of August 2007, $300 billion of leveraged finance loans made by banks is effectively “orphaned” - they can’t be sold off. One bank recently offered $1 billion to a client to walk away from an underwriting commitment where it stood to lose more if the transaction proceeded. Another bank, active until recently in making multi-billion dollar commitments to private equity transaction, told clients that “they were not in leveraged lending business any more”. It smacked of a day in the late 1980s when the then all powerful Japanese banks refused to participate in the leveraged financing of the United Airlines LBO ushering in the end of that era.

Keynes observed capital shifts “with the speed of the magic carpet … disorganizing all steady business”. The real economy effects are slower to emerge and more difficult to measure. Higher credit costs and tighter credit standards will affect all business. The US housing industry is badly affected with no immediate prospect of a quick recovery.

Private equity transactions in recent years were predicated on a combination of a growing economy, cheap debt and a buoyant stock market allowing the quick resale of the company. Weaker earnings and more expensive debt could lead to losses and distressed sales over time. Non-investment grade bond issuance over the last few years was concentrated in the weaker credit categories and is vulnerable to deterioration in economic conditions.

The fall in asset prices has “wealth” effects. US consumption, based on borrowing against the inflated values of financial assets, drives the export driven economies of Asia, Eastern Europe and Latin America. Lower commodity prices already point to slower global growth. While main street was trying the assess the fallout, Wall Street was already issuing “pink slips” by the thousands as banks and mortgage lenders shed staff.

The market anxiously waited for “the shoes to fall”, except it seemed the shoes were from Imelda Marcos’ collection.

Shell Games

Markets exaggerate the short-term impact and underestimate the long run impact of events. The new liquidity factories were based on the new age idea of “risk transfer”. The shell game requires three shells and a small, soft round ball, about the size of a pea. The pea is placed under one of the shells, then quickly the shells are shuffled around. Bets are taken from the audience on the location of the pea. It is a confidence trick used to perpetrate fraud. Through sleight of hand, the operator easily hides the pea, undetected by the victims. Risk transfer is the shell game of the credit markets; a short con, quick and easy to pull off.

Central banks believe that if banks sell off their risk then it is distributed widely reducing the chance of a crash. Banks frequently don’t sell off their real risks. For regulatory capital reasons, they sell off less risky loans. In a CDO, the bank typically takes all or a portion of the equity tranche. This is “hurt money” or the “skin in the game” to reassure other investors. Banks must hold the loans until they can be sold. If there is a market disruption and the bank is unable to sell then the risk remains with the bank.

The risk may also return to the bank via the back door. Where it acts as a prime broker –executing trades, settling transactions and financing hedge funds – the bank lends to investors using the CDO securities created as collateral. If the value of the securities falls and the hedge fund is unable to post additional margin to cover the loss then the bank is exposed to the risk of the securities. The bank assumes that it can sell the securities it is holding to pay itself back. There are few prime brokers - three dominate the business - concentrating the risk.

Banks provide “corporate credit cards” - standby lines of credit - to the conduit vehicles to cover funding shortfalls. If CP cannot be issued then the banks may be forced to lend against the assets that they have supposedly sold off. In the current crisis, some banks refused to lend arguing material changes in circumstances. Others foraged down the back of the sofa for any loose change to add to their dwindling liquidity to meet their commitments. Some bowed to the inevitable and took the assets back on to their balance sheets.

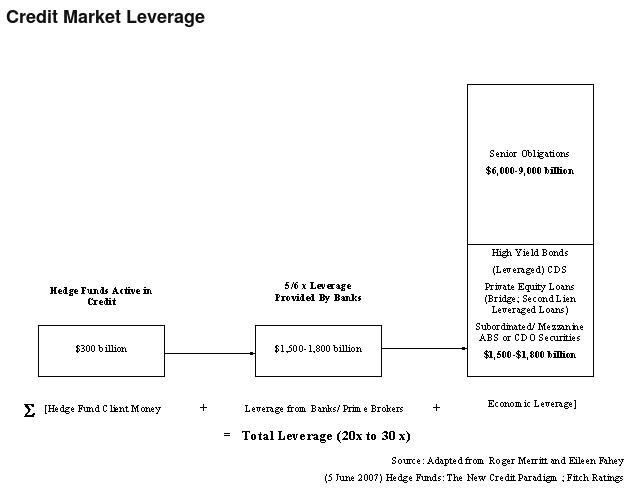

Credit risk moves from a place where it was regulated and observable to a place where it is less regulated and more difficult to identify. Around 60% of all credit risk is transferred to highly leveraged hedge funds that may be inadequately capitalised to bear the risk. Table 1 and Diagram 4 sets out the amount of leverage in modern credit markets – around one dollar of “real” capital supports between $20 and $30 of loans.

Table 1

Diagram 4

Hedge fund trading strategies create risk concentrations as they hunt in packs taking bets on the same events. Hedge funds investors can withdraw funds at relatively short notice, typically, one to three months. The hedge fund’s borrowings (via repos and derivatives supported by collateral) are short term – one day. Short-term money finances long-term assets making them vulnerable to a credit crisis. As the credit problems spread and hedge funds faced margin calls, one humorist wryly suggested that they meet capital calls using nickels, pennies, and quarters.

Banks set up hedge funds and invest in them. When a hedge fund gets into trouble there is commercial and reputational pressure to support the fund bringing the risk back into the bank. Financial innovation may not decrease risk but increase risk significantly in complex ways.

Ph.D’s (Piled Higher and Deeper)

There are now more models in financial markets than on catwalks. Trading models tell you when and what to buy and sell. Pricing models value any conceivable security. Risk models tell you how much you may loss. Meta-models tell you which model to use.

Investors increasingly don’t know what they are buying and what the security is worth. Traders say that the cost of what they sold is lower then what they paid for it; the price they paid is always lower than what the security is worth. Traders are smart and everyone else is stupid. Complex securities frequently don’t trade at all so market prices are rarely available. Understanding and valuing structured securities requires a higher degree in a quantitative discipline, a super computer and a vivid imagination.

The current credit crisis is, in part, a case of model failure. In the US mortgage market, automated credit assessments where information such as stated income or assets are not verified led to poor lending. At the time of the purchase, HSBC had trumpeted Household’s mortgage financing skills. Mention was made of hundreds of Ph.D.’s skilled at cutting and dicing mortgage risk. In hindsight, HSBC would have been better served by old fashioned, common sense bankers who could eyeball clients and decide who was likely to pay you back.

Complex Monte Carlo models used to model and rate CDO securities performed badly. Trading models used by quantitative hedge funds malfunctioned as prices became driven by liquidity and market regimes shifted. Models used to set trading limits and set collateral levels significantly underestimated risk as volatility increased.

The risk of simplified, sometimes untested, models is not new. In 1987, portfolio insurance contributed to the crash. In 1998, LTCM’s trading and risk models failed. Robert Merton articulated the problems precisely. “At times we can lose sight of the ultimate purpose of the models when their mathematics become too interesting. The mathematics of models can be applied precisely, but the models are not at all precise in their application to the complex real world. Their accuracy as useful approximations to that world varies significantly across time and place. The models should be applied in practice only tentatively, with careful assessment of their limitations in each approximation.” The speech was less than a year before the collapse of LTCM.

Missing The Mark

Asset values, profits and losses, risk calculations and collateral requirements all require the current market price of securities. Even staid accountants have embraced mark-to-market (“MTM”) as the basis for financial reporting. MTM assumes a market and a price. In volatile markets, liquidity becomes concentrated in government bonds, large well know stocks and listed derivatives. For anything that is not liquid, MTM means mark-to-model entailing “model risk”. The only price available is from the bank that sold the security to the investor in the first place defying concepts of independence and objectivity.

As the 2007 credit crisis unfolded, there was no liquidity for structured securities. There was only one marketmaker - the person who sold it to you in the first place. In a dealing room during a crisis, the first rule is do not answer phone calls from clients. The second rule is say “wrong number” if you accidentally pick up the phone.

Inability to price or trade means that fund managers cannot establish current portfolio values or allow withdrawals of investor money. This forced funds to suspend withdrawals. Prime brokers could not establish the value of collateral. Where investors failed to make “top up” margin calls, the prime brokers could not sell the collateral securing their loans. They couldn’t get back their money and were at risk of further falls in the value of securities.

Banks shared one objective - prevent the complex and illiquid securities being sold at a discount and pushing down prices in the market. If these securities actually traded then the lower market price would have to be used to calculate the mark-to-market value increasing losses and margin calls on already cash strapped investors. Asset values, profit and loss calculations and risk computations were in the running for major awards in literary fiction.

Unknown Unknowns

One trader summed it up using Donald Rumsfeld’s immortal words: the known known was that there were losses in sub-prime mortgages and anything related; the known unknown was that everybody knew that they did not know the full extent of the problem; the unknown unknown was that there could be other problems that we didn’t know about yet.

Financial crises now are less the result of economic downturns, geopolitical events or natural disasters and more the result of the structure and activity in financial markets. 9 Risk is now driven by the increasingly tight coupling of markets and the resulting complexity and interdependence.

Modern financial markets assume free flow of information and relative transparency. There was little or no knowledge of the extent of sub-prime losses, who was exposed and what were the links.

Sometimes, investors themselves couldn’t work out whether they had sub-prime exposure or not. In the early stage of the crisis Baudoin Prot, the chief executive of France's biggest bank, BNP Paribas, sought to reassure markets: “With only three funds, for a total of € 2 billion, which for one-third of the assets have some sub-prime, US sub-prime exposure. For us this is not a significant problem at this stage.” Within the week, BNP Paribas had to freeze payments from the funds as they were unable to obtain market prices or trade the CDO securities. An analyst assured me that Asian banks’ exposure to sub-prime losses was minimal. Within days, Chinese, Korean and Japanese banks announced large exposures to sub-prime. The stock markets wiped 30-50 times the potential losses off the share prices of the banks. The issue was that the banks did not know what they owned and what they could lose.

Diffusion of risk across the globe to unregulated investors subject to variable financial disclosure rule is inconsistent with transparency. Investors like hedge funds have steadfastly fought for increasing transparency and disclosure, except when it relates to their own activities. One central banker observed that in the good old days, there would have been no problem as the risk would be where it always was - at the banks.

Truth in Labeling

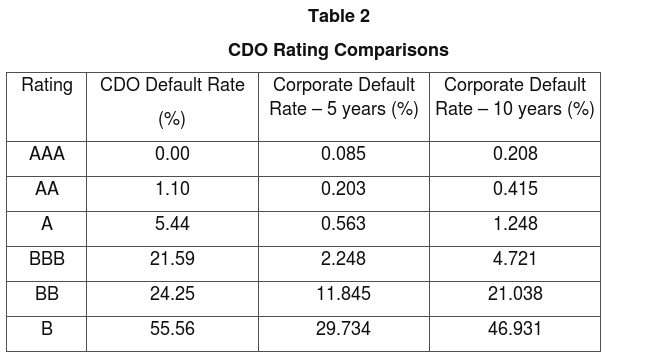

CDO ratings have been crucial to selling securities to investors. 30% and 50% of the revenue of the major rating agencies – Moody’s Investor Services; Standard & Poor; Fitch Ratings – come from rating structured securities, including CDOs.

Ratings are opinions of the likelihood of default of a particular security based on mathematical models, history and snake oil. Investors, some ignorant about how a rating is determined, ascribed magical properties to the alphabet soup of letters assigned to a security. Investors and bankers made assumptions about the stability of the rating. Rating was linked to pricing and used to set the amount of banks would lend against a particular security. Protected by expansive exclusion clauses, the agencies did not discourage these uses, instead promoted the wide use of ratings.

CDO rating anomalies abound.10 The number of defaults in the “BBB” class of CDO securities is not materially different from that on “BB” CDO securities (see Table 2). BBB is classified as investment grade while BB is not. Many investors can only purchase investment grade securities but in a CDO it seems the risks are the same. CDO security ratings also seem to be less stable than comparable rated corporate bonds. Likely reasons include model failure, input problems and a certain naivete in the application of these models to new markets. Bill Gross, from PIMCO, colorfully observed that in rating CDOs the agencies had been seduced by “hookers in six-inch stilettos”.

There are uncomfortable similarities in the relationship between investment banks and rating agencies and that between auditors and the companies they audit. Investment banks pay the rating agencies to rate the CDO securities. Investment banks and rating agencies work closely in structuring the transactions. Rating agency staff cross over to the “dark side” to work for investment banks. CDO ratings pay more than rating conventional bonds. Politicians in the USA and the European Union have started to focus on the role of rating agencies.

Notes:

1. CDO Default Rates are from Jian Hu, Richard Cantor and Gus Harris (March 2005) Default and Loss Rates of US CDOs: 1993-2003; Moody’s Investor Services at Figure 10.

2. Corporate Default Rates are from David Hamilton, Praveen Varma, Sharon Ou and Richard Cantor (March 2006) Default and Recovery Rates of Corporate Bond Issuers 1920-2005; Moody’s Investor Services at Exhibit 35.

Who’s Watching the Watchers ….

John Kenneth Galbraith observed that: “in central banking as in diplomacy, style, conservative tailoring, and an easy association with the affluent count greatly and results far much less.” Central bankers fueled the liquidity factories through excessive monetary growth and low interest rates. They championed financial innovation and “new age” finance theories. The risks of a diffuse, globally interlinked, highly leveraged financial system were ignored.

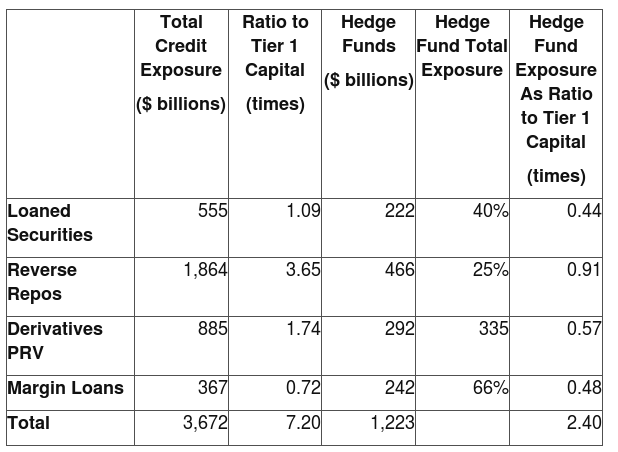

Regulators have presided over substantive changes in financial institution balance sheets and risks. The balance sheet of large banks and investment banks hold illiquid assets, such as private-equity investments, bridge loans, hedge funds investments, distressed debt and exotic derivatives. Derivative transactions with and loans to hedge funds through their prime broking operations have increased. Assets and exposures in “arbitrage” conduit vehicles and hedge funds outside regulated bank balance sheets have increased.

Table 3 sets out a recent analysis of major banks’ exposures relative to capital. While banks have increased capital and reduced reliance on short-term funding, the increase in risk is equally significant.

Table 3 - Hedge Fund Shares Of Prime Broker Counterparty Exposure

Notes:

1. Loaned securities refers to bank lends securities to hedge funds and others in order to short sell. The bank receives cash or other securities as collateral,

2. Reverse repurchase agreements refers to a form of secured lending where the bank buying securities from a hedge fund and others against a commitment to buy them back.

3. Derivatives positive replacement value (“PRV”) is the current value of the contract calculated as the cost to the bank of replacing the transactions where the bank is owed money. This is lower than and massively understates the notional value of derivative contracts (potential command over securities).

4. Margin loans refer to bank advances to hedge funds and other against collateral (usually cash and securities). This important activity is not separately disclosed by prime brokers. The figure is the total margin lending by members of the NYSE.

5. Tier 1 capital refers to shareholders funds but excluded most forms of subordinated debt and hybrid capital instrument.

6. Investment banks included in this analysis are (in alphabetical order): Bear Stearns; CitiGroup; Credit Suisse; Deutsche Bank; Goldman Sachs; JP Morgan; Lehman Brothers; Merill Lynch; Morgan Stanley; and UBS.

Source: Adrian Blundell-Wignall (2007) An Overview of Hedge Funds and Structured Products: Issues in Leverage and Risk; OECD

Banks also have increased trading risks, particularly in complex derivatives and structured investments. Constant Portion Portfolio Insurance (“CPPI”) products guarantee the return of capital to investors at a future date using a trading strategy similar to portfolio insurance. This requires continuously re-balancing of a portfolio of risky assets (usually shares and hedge fund investments) and cash. The trader is exposed to the risk of sharp changes in asset prices. It is unclear how these products and hedges will perform in volatile markets.

The Bank of International Settlements (“BIS”) in its 2007 annual report admitted that “our understanding of economic processes may be even less today than it was in the past”. Fundamental changes reshaping financial markets are needed. The temptation to seek a scapegoat (the brokers that sold sub-prime mortgages and rating agencies loom large) or a quick fix (lower interest rates) is ever present. The Fed has cut the discount rate. The Fed also clarified the rules – banks could pledge asset backed CP as collateral for funding at its discount window. Usually, only government securities are eligible. The Fed is effectively underwriting the credit risk and the liquidity of the financial system. It was arguably reverting to type bailing out banks and investors from poor decisions or irrational exuberance underwriting excessive risk taking.

John Maynard Keynes knew the problem well: “the difficulty lies not so much in developing new ideas as in escaping from old ones”. But as John Kenneth Galbraith observed: “faced with the choice between changing one’s mind and proving there is no need to do so, almost everyone gets busy on the proof.”

Credit Crunch

In Western societies, there is an increasing obesity problem, in part caused by poor diets that include fast food. A diet of cheap and excessive debt has created a bloated financial system.

Crash diets rarely work. The solution requires will power, a sensible but reduced food intake and exercise. In financial markets, the resolution requires regulatory will and an imposition of market disciplines on errant investors and banks. It also requires a sharp reduction in debt levels and addressing the problems of risk transfer, model risk and market transparency.

I am not hopeful that the required reassessment will occur. The current credit crunch will be the new wonder diet snack for financial markets. It will have some short term effects but leave the root cause untreated. As Charles Kindleberger noted in the opening sentence of his classic study (Maniacs, Panics and Crashs): “there is hardly a more conventional subject in economic literature than financial crises.”

© 2007 Satyajit Das. All rights reserved.

1. Gillian Tett of the Financial Times coined the phrase; see Gillian Tett “Should Atlas still shrug?” (15 January 2007) Financial Times

2. The phrase new liquidity factory was coined by Mohamed El-Erian.

3. See Joseph Mason and Joshua Rosener “How Resilient are Mortgage Backed Securities to Collateralised Debt Market Disruptions?” (13 February 2007)

4. See “Cracks in the façade” (22 March 2007) The Economist

5. See Merrit, Roger, Linnell, Ian, Grossman, Robert and Shiavetta, John (18 July 2005) Hedge Funds: An Emerging Force in Global Credit Markets; Fitch Ratings, Special Report, New York

6. See Peter Schwartz and Peter Leyden “The Long Boom: A History of the Future, 1880-1920” (July 1997) Wired

7. See E.W. Howe, Sinner Sermons

8. See McKinsey Global Institute (January 2007) Mapping The Global Capital Markets – Third Annual Report

9. See Woody Brock (2002) The Transformation of Risk: Main Street versus Wall Street

10. See Arturo Cifuentes and Georgios Katsaros “CDO Ratings: Chronicle of a Disaster Foretold” (4 June 2007) Total Securitisation 11-12

...

Understanding and valuing structured securities requires a higher degree in a quantitative discipline, a super computer and a vivid imagination.

...

Diffusion of risk across the globe to unregulated investors subject to variable financial disclosure rule is inconsistent with transparency. Investors like hedge funds have steadfastly fought for increasing transparency and disclosure, except when it relates to their own activities. One central banker observed that in the good old days, there would have been no problem as the risk would be where it always was - at the banks.

...

John Kenneth Galbraith observed that: “in central banking as in diplomacy, style, conservative tailoring, and an easy association with the affluent count greatly and results far much less.” Central bankers fueled the liquidity factories through excessive monetary growth and low interest rates. They championed financial innovation and “new age” finance theories. The risks of a diffuse, globally interlinked, highly leveraged financial system were ignored.

...

Crash diets rarely work. The solution requires will power, a sensible but reduced food intake and exercise. In financial markets, the resolution requires regulatory will and an imposition of market disciplines on errant investors and banks. It also requires a sharp reduction in debt levels and addressing the problems of risk transfer, model risk and market transparency."

Credit Crunch – The New Diet Snack for Financial Markets

By Satyajit Das

September 5, 2007

Source

Satyajit Das works in the area of financial derivatives and risk management. He is the author of a number of key reference works on derivatives and risk management and is the author of Traders, Guns & Money: Knowns and Unknowns in the Dazzling World of Derivatives (2006, FT-Prentice Hall).

Living in the Kaliyuga …

Inflexion points in financial markets are difficult to identify. As Yogi Berra observed: “making predictions is difficult, especially about the future”.

In Indian mythology, we are in the Age of Kali - the last age. The world ends when Kali dances the dance of death. There are no such clear markers in markets. Recently, we came close - Jim Cramer, a CNBC pundit, launched a “we’re in Armageddon” tirade on air. Embattled Bear Stearns’ CFO Samuel Molinaro pleaded: “I’ve been out here for 22 years, and this is as bad as I’ve seen it in the fixed-income markets.” Kali had begun to shake her booty. The credit bubble was finally deflating.

In 2007, householders in “cabbage-ville USA” (an English fund manager’s term) failed to make repayments triggering a global credit crisis. Markets ruminated about “a re-pricing of risk”. The faux “business as usual” calm masked the fact that the problems threaten to be the single largest credit crisis since the Savings and Loans collapse in the USA in the 1980s.

The early 2000s were a period of “too much” and “too little” – too much liquidity, too much leverage, too much complex financial engineering, too little return for risk, too little understanding of the risks. Steven Rattner (from hedge fund Quadrangle Group) summed it up in the pages of the Wall Street Journal: “No exaggeration is required to pronounce unequivocally that money is available today in quantities, at prices and on terms never before seen in the 100-plus years since U.S. financial markets reached full flower.” Traditional money fueled by loose monetary policy, excessive capital flows and now turbo-charged by “financial engineering” lies at the heart of the current credit crisis.

Structured Credit - Supersize My Debt!

Candyfloss (cotton candy or fairy floss) - spun sugar - consists mostly of air. It is the quintessential experience of a visit to a fairground. New financial technology is “candy floss” money 1- money spun out and expanded into ever larger servings. Derivatives, securitisation and collateralised lending allow fundamental changes in credit markets and leverage.

Derivatives – highly leveraged commercial bets on movements in prices of interest rates, currencies, shares and commodities - can be used to manage or create risk. Investors increasingly use derivatives to increase risk to earn higher returns. As at the end of 2006, derivative outstandings were around $485 trillion. In comparison, total global Gross Domestic Product is around $ 60 trillion. Derivative trading created additional liquidity and leverage.

Derivatives on credit instruments are a relatively recent innovation. A credit default swap (“CDS”) is credit insurance on a specific company. The buyer of protection (usually a bank who has lent money to the company) pays the seller of protection (usually an investor) a fee. In return, the seller of protection covers the bank buying protection against losses should the company go bankrupt. CDOs are steroid-fueled mortgage loan securitisations. A portfolio of loans, bonds or mortgages is assembled. Interest and principal from the underlying portfolio is used to make payments on the CDO securities issued to investors.

In a CDS contract, unlike a loan or bond, the investor is not required to pay the full face value. CDS volumes are not limited to the outstanding amount of debt. General Motors has around US$130 billion of debt. CDS volumes on GM are around 6 to 10 times that. CDSs allowed the credit markets to “supersize” trading volumes.

In CDOs, the bank uses the dexterity of the Iron Chef to cut and dice the risk of the underlying loans. “Tranching” allows the creation of different CDO securities - equity, mezzanine and senior debt. Equity receives high returns and bears the most risk. If there are losses on the portfolio of loans then equity takes the first losses. The senior note holders take the least risk as they are first in line to get paid and last to lose. They get low returns but more than on comparable traditional securities. Mezzanine (code for subordinated debt) is somewhere in between. Tranching is used to alter credit ratings on portfolios of A/ BBB loans to manufacture AAA/ AA securities.

CDOs concentrate risk and increase the potential gain or loss for a given event. CDOs are based on “diversified” underlying portfolios; e.g. a $1,000 million portfolio made up of 100 loans of $10 million each. Assume that if any of the 100 firms goes bankrupt, you lose $6 million (60% of $10 million). If the equity tranche is $20 million (2%), then the investor takes the risk of the first 3 firms to go bankrupt out of the 100 firms in the portfolio ($20 million of losses divided by $ 6 million). The investor’s risk is not diversified; it is taking the risk on the 3 worst firms out of the 100 in the portfolio.

If the investor invested $20 million in the 100 loans ($200,000 per corporation calculated as $20 million divided by 100), then 3 defaults in the portfolio would result in a loss of only $0.36 million (loss of $120,000 per company (60% of $200,000) times 3). In a CDO, if there are the same 3 losses then the equity investor losses $20 million. The leverage to default is 56 times ($20 million versus $0.36 million). Frequently, the holder of the equity tranche borrows to fund its stake further increasing leverage. A regulated bank can leverage around 12 ½ times. CDOs concentrate credit risk – the term is “toxic waste”.

The structured credit market has supersized debt levels using techniques of staggering complexity, incomprehensible to all but a small group of practitioners. The market was so “like hot” that one professional confessed that even his headhunter had been recruited into a structured credit role at an investment bank.

Would you like debt with that?

Repurchase agreements or “repos” (secured lending against government securities) and margin loans (lending secured against stocks) are well established. Now, investors use repos to raise substantial amounts against any security or instrument, including distressed debt.

Investors routinely structure asset purchases as a total return swap (“TRS”). The investor receives the return on the asset (income and increases in price) in return for paying the cost of holding the asset (decreases in price and the funding cost of the dealer). The investor posts a modest initial margin or “haircut” and promises to post more cash if the value of the asset declines. The trader has bought the asset with money borrowed from the dealer with which it entered into the TRS. Favorable regulatory rules, optimistic views of liquidity (the collateral must be sold if the borrower fails to pay) and faith in the models used to set the margins drives aggressive use of collateral increasing available liquidity and leverage.

Banks have also institutionalized the collateral game in a plethora of off-balance sheet structures – arbitrage or conduit vehicles; structured investment vehicles (“SIVs”). The vehicles purchase high quality securities like AAA or AA rated CDOs and fund them with short-term borrowings (usually, commercial paper (“CP”) issued to money market funds). $1.2 trillion or 53% of the $2.2 trillion commercial paper in the US market is now asset backed, around 50% by mortgages. When investors now buy assets, the dealers automatically ask: “would you like debt with that?”

The New Liquidity Factory 2

Banks traditionally wrote and funded their loans. In the new money game, banks “originate” loans, “warehouse” them on their balance sheet for a short time and then “distribute” them to investors using CDOs. Banks require less capital, as they don’t hold the loan for its full term. The process encouraged declines in credit standards. The game relies on the ongoing liquidity of the market for securitised debt.

When the loans are sold, the bank effectively receives the difference between the interest on the loan and the return demanded by the investor “upfront”. As loans are sold off, more loans must be written. Ever larger volumes are necessary to maintain profitability forcing banks to rely on brokers. In the new money game, banks increased loan volumes, reduced capital available to absorb risk and lowered the credit quality of their loans all at the same time.

Insurance companies, pension funds, asset managers, banks, and private clients are buyers of credit risk. Hedge funds moved into the credit markets in search of higher returns based on leveraged structured credit instruments. The high returns came with additional risks – a lack of liquidity and complexity of the securities. Buyers from Switzerland to Slovakia, Boston to Beijing bought up credit risk. A feature of credit investing was that the complexity and risk of structures was inversely related to the understanding of the investor being sold it.

In the new liquidity factory, investors did the borrowing - hedge funds borrowed against investments; traders borrowed cheap money (especially yen at zero interest rates) to fund high yielding assets in the famous carry trade. Financial engineering disguised leverage so that an investor’s balance sheet today does not tell you the amount of leverage being employed.

The new liquidity factory is self-perpetuating. If you bought assets with borrowings then as the asset went up in price you borrowed more money against it. In an accelerating spiral, asset prices rise as debt fuels demand for the asset. Higher prices decrease the returns forcing the investors to borrow more to increase returns. Bankers became adept at stripping money out of existing assets that had appreciated in price, such as homes. In the USA, UK and Australia – the fast debt nations - home equity borrowing funded a frantic debt addiction.

By the early 2000s, the new liquidity factory had created a money pyramid that had no parallel in history. Diagram 1 sets out the money pile in modern markets. The tsunami of debt fueled price increases in financial assets - debt, equity, property, infrastructure. The current market volatility is not simply a correction in prices but this gigantic liquidity bubble unwinding.

Diagram 1 - The New Liquidity Factory

Lying NINJA Mortgagors

A German banker recently accosted me: “vhat does a poor American defaulting in Looneyville, West Virginia have to do vith me?” There were also defaults in Gravity Iowa, Mars Pennsylvania, Paris Texas, Venus Texas, Earth Texas, and Saturn Texas.

Deregulation, abundant liquidity and rising house prices encouraged lenders to target less affluent borrowers with poor credit histories who have long been excluded from the American dream of home ownership. Sub-prime and Alt A housing loans included “innovations." 3

Loan to value ratio (“LVR”) – traditional mortgages provide 70-80% of appraised value. Sub-prime mortgages had more aggressive LVRs including “negative” equity loans (the lender is lending more than the value of the house). Undisclosed “piggyback” loans and silent second mortgages eliminated any deposit requirement.

· Interest payments – sub-prime mortgage repayments sometimes don’t cover interest on the loan. In a negative amortisation loan, the principal actually increases as interest is not covered. There were “teaser’ rates – 2/ 28 mortgages where there are artificially low rates (as low as 1%) for the first 2 years with the loan interest being reset at the end of the “honeymoon” period. Sub-prime mortgages were adjustable rate mortgages (“ARMs”) rather than the more typically fixed rate mortgages.

· Jumbo loans – these were large loans (above $417,000) needed to finance more expensive houses.

· Credit review and loan underwriting standards – the mortgage industry increasingly relied on credit scoring models. Statements of income and assets are not checked. Outsourcing mortgage origination to brokers and shifting of risk to investors led to a systematic decline in underwriting standards.

· Purpose of loan –a high portion of sub-prime was directed to monetisation of the equity in existing homes; between 2000 and 2005, total mortgage equity withdrawal increased from $289 billion to $900 billion.

Around 2003/ 2004, the housing market began to slow. Banks and brokers maintained volumes at the expense of even weaker standards. LVRs rose and documentation requirements collapsed. Demand for long term high-yielding assets from investors fueled the securitisation process that the sub-prime market relied upon. By 2007, the sub-prime market accounted for 20% of new mortgages and 10% of all mortgage debt.

Francois Rabelias, the French author, observed in the 16th Century: “debts and lies are generally mixed together.” NINJAs (“no income, no jobs or assets”) able to sign their name could buy a house without any money. In 2006, Casey Serin, a 24-year old web designer from Sacramento, bought seven houses in five months with US$2.2 million in debt. He lied about his income on “no document” loans. He had no deposit. In 2007, three of his houses were repossessed. The others face foreclosure. Serin’s website - www.Iamfacingforeclosure.com - has become the symbol of the excesses of the sub-prime mortgage market. 4

Hedge funds used leverage to “enhance” returns on sub-prime debt. Diagram 2 shows how a hedge fund uses $10 million to take the risk of the first $60 million of losses on a $850 million portfolio.5

Diagram 2

A Gradual and Sudden Death

The “Goldilocks” economy led one commentator in 1997 to assume that the business cycle had been abolished.

“We are watching the beginning of a global economic boom on a scale never experienced before. We have entered a period of sustained growth that could double the world’s economy every dozen years and bring increasing prosperity for – quite literally – billions of people on the planet. We are riding the early waves of a 25-year run of a greatly expanding economy that will do much to solve seemingly intractable problems like poverty and to ease tensions throughout the world. And we’ll do it without blowing the lid of the environment.”6

Unfortunately, interest rates increased sharply in the US. Central banks tightened liquidity as inflation rose driven by higher oil prices, increasing costs in emerging countries and infrastructure constraints. US house prices stalled and then fell. Delinquencies in sub-prime mortgages reached 15% and in some types of loans approached 30%. Defaults rose. at an uncomfortable 45’ gradient.

In 2006, an asset based securities credit index had been introduced to provide some transparency to the opaque CDO and mortgage markets. The ABX.HE (Asset backed Securities Home Equity) entailed five separate indexes (AAA, AA, A, BBB, BBB-) referencing similarly rated tranches of 20 securitisation transactions. The BBB- 2006 index collapsed from around 100 to initially 60-70% of face value to its current level of around 30-40%. It was, according to Luiz Inácio Lula da Silva (“Lula”), President of Brazil, “an eminently American crisis” caused by people trying to make a lot of “third-class money”.

Like engine oil, credit lubricates and keeps the financial motor running. The oil was leaking out rapidly; the engine was seizing up. Sub-prime mortgage lenders closed as business dried up. Investments in the riskier tranches of the securitised mortgage pools were worthless. Investors in the “safe”, higher rated – AAA and AA tranches – had real problems In a typical securitisation, actual losses on the underlying mortgages pool would need to rise above 15-30% before they suffered losses. AAA tranches were quoted (if you could find a quote!) at between 80-90% of face value. AA and A were lower again.

The AAA rating of senior tranches is based on layers of subordinated securities to absorb initial losses. As expected losses mounted and the lower layers were eaten away, the AAA rating of the senior tranche fell leading to mark-to-market losses – i.e. what the security is worth if sold today.

If the investor ignored the current (mark-to-market) value then the investor was still unlikely to actually lose money. Lower ratings forced investors to sell as the securities did not comply with investment guidelines triggering losses. Hedge funds who borrowed against the securities faced margin calls as the values fell. The lenders tightened lending conditions reducing leverage and increasing the cost. “No man’s credit was now as good as his money”. 7

The sub-prime problem was initially a “specific problem” and “contained”. It was neither. It spread quickly and efficiently – the word “contagion” appeared. By August 2007, credit markets had just about ceased to function. A veteran commentator – Ian Kerr - compared the current credit crunch to death from radiation – CDOs, particularly those with sub-prime exposure, now stood for Chernobyl Death Obligations!

Bear in the Woods

Two investors see a bear in the woods. One investor starts to run. “You can’t outrun a bear,” the other investor shouts. “I can outrun you!” responds the running investor. Investors and financial institutions now wanted to get their money out before the cash vanished. Diagram 3 sets out how selling is exaggerated in a highly leveraged world.

Diagram 3

The United States absorbs around 85% of total global capital flows, or over $500 billion each year. Asia and Europe were the world’s largest net suppliers of capital, followed by Russia and the Middle East. Cross border debt flows funded the US government debt (up $400 billion) and a rapid expansion in US private debt (up $1.3 trillion). A key growth area was asset-backed securities (“ABS”), including mortgage-backed securities (“MBS”), reflecting the strong US housing market and high levels of home-equity lending.8 Global money funded the US debt binge and now global investors suffered losses.

Exposure started to show up in unlikely places via asset backed CP – money market funds. One institution disclosed that CDOs and subprime mortgages were classified as “cash and short term” on its balance sheet. Structured funding vehicles were unable to issue ABS backed CP. They drew on standby funding arrangements. Banks refused to fund arguing material changes in circumstances. Others had to forage down the back of the sofa for any loose change to add to their dwindling liquidity.

Reduced leverage and higher costs of funding affected hedge funds. Quantitative funds suffered large losses as forced selling and a liquidity driven market caused models to fail. Hedge fund investors, concerned about declines in returns and sharp falls in value, lodged redemption requests forcing selling. Goldman Sachs was forced to step in to offer liquidity support to one of its funds.

Overheated equity markets fell despite strong corporate earnings and a growing economy on concerns about less abundant and higher priced debt. Stock values exaggerated by the possibility of debt fuelled private equity bids fell sharply. Financial stocks fell as the losses, bailout costs and loss of future earnings was factored in. Investors regretted not taking Will Rogers advice: “don't gamble; take all your savings and buy some good stock and hold it till it goes up, then sell it. If it don’t go up, don’t buy it.”

Market credit spreads and margins rose sharply. There was a flight to quality – government securities and cash. Liquidity vaporized as fear about counterparty default meant that normal transactions between financial institutions became difficult. Risk lending dried up. AAA rated non sub-prime mortgage-backed securities could not be placed.

There is no difference between a run on a bank and shutdown of access to funding from the capital markets. US mortgage lenders faced old-fashioned runs. Central banks pumped money into the system. The Fed cut the discount rate. Four major US banks used the discount window: “to encourage its use by other financial institutions”. They did not need cash. It was a sign of strength. In the words of financial historian, Charles Geisst, it was : “like someone from the Upper East Side being seen in .. Wal-Mart”.

The problem was credit risk not liquidity. Lack of information and diffusion of risk meant that no one was certain who had exposure to what or to whom. EBC governor Jean-Claude Trichet pleaded for everybody “to keep their composure”. It was reminiscent of Emperor Hirohito’s response to the bombing of Hiroshima: “the War situation has developed not necessarily to Japan’s advantage.”

Waiting for the Shoe to Fall…

A pyroclastic flow is a part of volcanic eruptions consisting of lethal currents of Tephra (hot 1000 degrees Celsius gas, ash and rock) travelling at up to 700 km/hour. Pompeii was famously engulfed by pyroclastic flows in AD 79. The sub-prime losses had morphed into a fully-fledged “credit crunch”, the pyroclastic flow of financial markets.

Hedge funds faced substantial redemption requests especially from funds-of-funds in charge of allocating hot money in the coming months. Interest rates on large volumes of sub-prime mortgages were due to increase (by 3-4%) in 2008. The impact on delinquencies and losses were unknown.

The same model as sub-prime is used for leveraged funding in private equity, infrastructure and property financing. Banks underwrote the loans, warehoused them and then repackaged and distributed them to investors in the form of CDOs. Deterioration in credit standards was evident. “Covenant lite” loans where the borrower did not agree to normal financial restrictions had become fashionable. “Toggle” loans where borrowers could pay in cash interest using new debt (Pay-In-Kind or PIK securities) abounded.

The same model as sub-prime is used, worryingly, for funding highly leveraged private equity, infrastructure and property transactions. As of August 2007, $300 billion of leveraged finance loans made by banks is effectively “orphaned” - they can’t be sold off. One bank recently offered $1 billion to a client to walk away from an underwriting commitment where it stood to lose more if the transaction proceeded. Another bank, active until recently in making multi-billion dollar commitments to private equity transaction, told clients that “they were not in leveraged lending business any more”. It smacked of a day in the late 1980s when the then all powerful Japanese banks refused to participate in the leveraged financing of the United Airlines LBO ushering in the end of that era.

Keynes observed capital shifts “with the speed of the magic carpet … disorganizing all steady business”. The real economy effects are slower to emerge and more difficult to measure. Higher credit costs and tighter credit standards will affect all business. The US housing industry is badly affected with no immediate prospect of a quick recovery.

Private equity transactions in recent years were predicated on a combination of a growing economy, cheap debt and a buoyant stock market allowing the quick resale of the company. Weaker earnings and more expensive debt could lead to losses and distressed sales over time. Non-investment grade bond issuance over the last few years was concentrated in the weaker credit categories and is vulnerable to deterioration in economic conditions.

The fall in asset prices has “wealth” effects. US consumption, based on borrowing against the inflated values of financial assets, drives the export driven economies of Asia, Eastern Europe and Latin America. Lower commodity prices already point to slower global growth. While main street was trying the assess the fallout, Wall Street was already issuing “pink slips” by the thousands as banks and mortgage lenders shed staff.

The market anxiously waited for “the shoes to fall”, except it seemed the shoes were from Imelda Marcos’ collection.

Shell Games

Markets exaggerate the short-term impact and underestimate the long run impact of events. The new liquidity factories were based on the new age idea of “risk transfer”. The shell game requires three shells and a small, soft round ball, about the size of a pea. The pea is placed under one of the shells, then quickly the shells are shuffled around. Bets are taken from the audience on the location of the pea. It is a confidence trick used to perpetrate fraud. Through sleight of hand, the operator easily hides the pea, undetected by the victims. Risk transfer is the shell game of the credit markets; a short con, quick and easy to pull off.

Central banks believe that if banks sell off their risk then it is distributed widely reducing the chance of a crash. Banks frequently don’t sell off their real risks. For regulatory capital reasons, they sell off less risky loans. In a CDO, the bank typically takes all or a portion of the equity tranche. This is “hurt money” or the “skin in the game” to reassure other investors. Banks must hold the loans until they can be sold. If there is a market disruption and the bank is unable to sell then the risk remains with the bank.

The risk may also return to the bank via the back door. Where it acts as a prime broker –executing trades, settling transactions and financing hedge funds – the bank lends to investors using the CDO securities created as collateral. If the value of the securities falls and the hedge fund is unable to post additional margin to cover the loss then the bank is exposed to the risk of the securities. The bank assumes that it can sell the securities it is holding to pay itself back. There are few prime brokers - three dominate the business - concentrating the risk.

Banks provide “corporate credit cards” - standby lines of credit - to the conduit vehicles to cover funding shortfalls. If CP cannot be issued then the banks may be forced to lend against the assets that they have supposedly sold off. In the current crisis, some banks refused to lend arguing material changes in circumstances. Others foraged down the back of the sofa for any loose change to add to their dwindling liquidity to meet their commitments. Some bowed to the inevitable and took the assets back on to their balance sheets.

Credit risk moves from a place where it was regulated and observable to a place where it is less regulated and more difficult to identify. Around 60% of all credit risk is transferred to highly leveraged hedge funds that may be inadequately capitalised to bear the risk. Table 1 and Diagram 4 sets out the amount of leverage in modern credit markets – around one dollar of “real” capital supports between $20 and $30 of loans.

Table 1

Diagram 4

Hedge fund trading strategies create risk concentrations as they hunt in packs taking bets on the same events. Hedge funds investors can withdraw funds at relatively short notice, typically, one to three months. The hedge fund’s borrowings (via repos and derivatives supported by collateral) are short term – one day. Short-term money finances long-term assets making them vulnerable to a credit crisis. As the credit problems spread and hedge funds faced margin calls, one humorist wryly suggested that they meet capital calls using nickels, pennies, and quarters.

Banks set up hedge funds and invest in them. When a hedge fund gets into trouble there is commercial and reputational pressure to support the fund bringing the risk back into the bank. Financial innovation may not decrease risk but increase risk significantly in complex ways.

Ph.D’s (Piled Higher and Deeper)

There are now more models in financial markets than on catwalks. Trading models tell you when and what to buy and sell. Pricing models value any conceivable security. Risk models tell you how much you may loss. Meta-models tell you which model to use.

Investors increasingly don’t know what they are buying and what the security is worth. Traders say that the cost of what they sold is lower then what they paid for it; the price they paid is always lower than what the security is worth. Traders are smart and everyone else is stupid. Complex securities frequently don’t trade at all so market prices are rarely available. Understanding and valuing structured securities requires a higher degree in a quantitative discipline, a super computer and a vivid imagination.

The current credit crisis is, in part, a case of model failure. In the US mortgage market, automated credit assessments where information such as stated income or assets are not verified led to poor lending. At the time of the purchase, HSBC had trumpeted Household’s mortgage financing skills. Mention was made of hundreds of Ph.D.’s skilled at cutting and dicing mortgage risk. In hindsight, HSBC would have been better served by old fashioned, common sense bankers who could eyeball clients and decide who was likely to pay you back.

Complex Monte Carlo models used to model and rate CDO securities performed badly. Trading models used by quantitative hedge funds malfunctioned as prices became driven by liquidity and market regimes shifted. Models used to set trading limits and set collateral levels significantly underestimated risk as volatility increased.

The risk of simplified, sometimes untested, models is not new. In 1987, portfolio insurance contributed to the crash. In 1998, LTCM’s trading and risk models failed. Robert Merton articulated the problems precisely. “At times we can lose sight of the ultimate purpose of the models when their mathematics become too interesting. The mathematics of models can be applied precisely, but the models are not at all precise in their application to the complex real world. Their accuracy as useful approximations to that world varies significantly across time and place. The models should be applied in practice only tentatively, with careful assessment of their limitations in each approximation.” The speech was less than a year before the collapse of LTCM.

Missing The Mark

Asset values, profits and losses, risk calculations and collateral requirements all require the current market price of securities. Even staid accountants have embraced mark-to-market (“MTM”) as the basis for financial reporting. MTM assumes a market and a price. In volatile markets, liquidity becomes concentrated in government bonds, large well know stocks and listed derivatives. For anything that is not liquid, MTM means mark-to-model entailing “model risk”. The only price available is from the bank that sold the security to the investor in the first place defying concepts of independence and objectivity.

As the 2007 credit crisis unfolded, there was no liquidity for structured securities. There was only one marketmaker - the person who sold it to you in the first place. In a dealing room during a crisis, the first rule is do not answer phone calls from clients. The second rule is say “wrong number” if you accidentally pick up the phone.

Inability to price or trade means that fund managers cannot establish current portfolio values or allow withdrawals of investor money. This forced funds to suspend withdrawals. Prime brokers could not establish the value of collateral. Where investors failed to make “top up” margin calls, the prime brokers could not sell the collateral securing their loans. They couldn’t get back their money and were at risk of further falls in the value of securities.

Banks shared one objective - prevent the complex and illiquid securities being sold at a discount and pushing down prices in the market. If these securities actually traded then the lower market price would have to be used to calculate the mark-to-market value increasing losses and margin calls on already cash strapped investors. Asset values, profit and loss calculations and risk computations were in the running for major awards in literary fiction.

Unknown Unknowns