(USA) Stage Two of the Mortgage Collapse - By Dr. Housing Bubble

Posted by ProjectC

Stage Two of the Mortgage Collapse: $500 Billion in Pay Option ARMs Meet the Piper in 2008 with 60 Percent Being in California.

By Dr. Housing Bubble

June 14th, 2008

Source

The next stage of the mortgage debacle is only starting to rear its ugly head and all early signs tell us that this is going to be even worse than the subprime mortgage collapse. We need to remember that the subprime mortgage debacle was only one facet of a global debt boom that has taken a stranglehold over the industrialized world. The United Kingdom is now starting to realize that even they are going to face a housing meltdown. Yet there is still a perception out there from pundits and those in the media that this housing meltdown was caused purely by subprime loans, which could not be anything further from the truth.

Many understand that this is a debt bubble and not only a collapse fueled by the subprime market in which low-income people bought overpriced homes. That in fact is a big player in this mess but many who once thought they were “prime” are going to be realizing there is nothing prime about them. Welcome to the even uglier side of things which is only in stage one at the moment. We now enter the Pay Option ARM debacle:

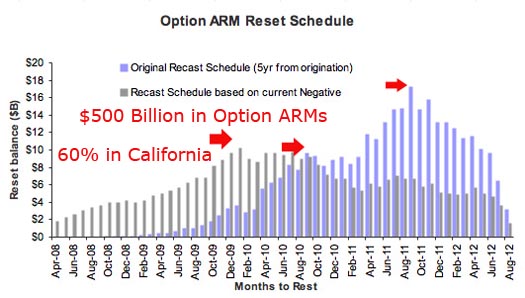

The most ominous sign of the above chart is the following:

-$500 Billion in total Pay Option ARMs outstanding in the U.S.

-60 Percent of these issued to folks in California

The Pay Option ARM is one of the most poorly construed mortgage product ever to face this planet. It was a pathetic attempt to allow a larger majority of Americans to have a piece of the great American credit ponzi scheme. Many of these loans give you the following pay options on a mortgage:

-Fully Amortizing 30-year payment - you pay both principal and interest on a 30-year schedule

-Fully Amortizing 15-Year Payment - you pay both principal and interest on a 15-year schedule

-Interest-Only payment - covers only the interest portion of the mortgage and does not pay down principal

-Minimum Payment - the most widely picked option in which your payment is set for 12 months at an introductory rate (remember those absurd intro rates?). After that, payment changes are made annually and a payment cap limits how much it can increase or decrease each year.

Just to show you how financially destructive these mortgage products will be let us look at a $500,000 loan with a teaser 1.25% intro rate:

*Source: http://mortgage-x.com

The loan if it were to be paid in 30-years carries a $3,010 monthly principal and interest payment while the intro teaser rate only required the owner to pay $1,666 per month deferring a large amount of the payment to a later date. You may be wondering, “well I’m sure only a handful of people opted to pay the minimum payment right?” Wrong.

“(Businessweek 2006) Now the signs of excess are crystal clear. Up to 80% of all option ARM borrowers make only the minimum payment each month, according to Fitch Ratings. The rest of the money gets added to the balance of the mortgage, a situation known as negative amortization. And once balances grow to a certain amount, the loans automatically reset at far higher payments. Most of these borrowers aren’t paying down their loans; they’re underpaying them up.

Yet the banking system has insulated itself reasonably well from the thousands of personal catastrophes to come. For one thing, banks can sell some of their option ARMs off to Wall Street, where they’re packaged with other, better loans and re-sold in chunks to investors. Some $182 billion of the option ARMs written in 2004 and 2005 and an additional $83 billion this year have been sold, repackaged, rated by debt-rating agencies, and marketed to investors as mortgage-backed securities, says Bear, Stearns & Co. (BSC )Banks also sell an unknown amount of them directly to hedge funds and other big investors with appetites for risk.

The rest of the option ARMs remain on lenders’ books, where for now they’re generating huge phantom profits for some lenders. That’s because, according to generally accepted accounting principles, or GAAP, banks can count as revenue the highest amount of an option ARM payment — the so-called fully amortized amount — even when borrowers make only the minimum payment. In other words, banks can claim future revenue now, inflating earnings per share.”

And for those of you who say we didn’t see this coming, that paragraph was pulled from a Businessweek article in 2006 title “nightmare mortgages.” Of course, Wall Street is no longer buying this crap so that $500 billion is going to implode and no one is going to stop it. Also, you need to remember that 60 percent of that mortgage portfolio of Pay Option ARMs is here in sunny California making us confront a $300 billion time bomb.

80% only made the minimum payment on these toxic waste products. I’ll draw your attention once again to that new chart recently released by Businessweek. What you’ll notice is that the gray bars are a better indicator of how quickly we will face this implosion since only a small minority were actually paying either the interest only or the 30-year options. California as a state is now down 30 percent in one-year and many niche markets are going to face 40 or even 50 percent drops. This will prove to be a bigger hit on the California housing market as we will see in the upcoming months.

Many of these mortgages now have larger balances! That is the absurdity of these mortgage products. If you really think about it, the minimum payment will actually increase the underlying amount you owe almost assuming your home will appreciate in the Wonderland reality of many homeowners and lenders. Now we have a somewhat cruel fate in which California median prices are crashing while many of these option ARM products have been slowly growing in the past few years. That is why lenders such as WaMu, Wachovia, and Countrywide who specialized in these toxic waste products are down by:

WM: down 84% from 6/14/2007

CFC: down 87% from 6/14/2007

WB: down 65% from 6/14/2007

Why do you think these companies are down so much? Aside from the subprime collapse they have seen nothing in regards to the option ARM debacle that is squarely facing them. $300 billion in mortgages alone in California that are worth so much less! Let us assume that these products are now only worth half of that $300 billion. That means California alone, not even counting the other $200 billion out there is going to hurt many direct lenders or Wall Street firms via writedowns by $150 billion with an almost guarantee given the 30 percent market decline. Let us do a quick market cap calculation of these 3 sample companies:

Marketcap as of 6/14/2008:

WM: $7.02 billion

CFC: $2.82 billion

WB: $38.89 billion

Total: $48.73 billion

Bwahaha! There combined marketcap is only about a third of the losses of pay Option ARMs which one state (California) will be facing! What if we factor that other $200 billion which undoubtedly will be facing losses as well given the nationwide scope of this housing debacle? Of course there are other lenders out there who dished out these toxic products but the above 3 were major players. Now you know why these institutions are off by ridiculous amounts. If you simply do the basic accounting and take the pulse of the market, you know that this has the potential of flooding lenders with a stream of losses for a few more years or until they go under. Take a look at the distress numbers for California last month:

May 2008:

NODs: 41,965

NTS: 9,728

REOs: 20,237

Total for California: 71,930

Nationwide total: 261,255

California makes up 27.5% of all foreclosure filings in May of 2008. Just to give you an idea how bad things are getting in California let us look at the stats for May of 2006:

May 2006:

NODs: 7,794

NTS: 804

REOs: 138

Total for California: 8,736

Nationwide total: 92,746

*Source: Realtytrac

So only two years ago, California made up 9.4% of all nationwide foreclosure filings and now we stand at 27.5%. This is how quickly things are coming apart at the seams and we haven’t even seen the first peak of option ARM recasts which should occur in October through December of this year. If you don’t think that $500 billion is a lot just wait until this summer selling season falls flat on its face for California. Fall and winter are going to be brutal.

Many of these owners are going to be highly tempted to moonwalk away from their mortgages. Does Bank of American really want to assume this option ARM time bomb? They are scheduled to close their deal with Countrywide sometime in the third quarter yet I simply do not see how they avoid astronomical losses on the current mortgage portfolios and REO properties. Unless California suddenly goes into another bubble and prices start going up, we are in for a tough few years and the current California multi-billion dollar budget short fall isn’t pretty either. Keep in mind the California budget which has now been revised to a $17 billion short fall is going to force us to make some hard decisions. Either raise taxes to plug budget gaps or cut spending (aka jobs) and only increase the unemployment numbers and thus depress the economy further.

No matter how you slice it, California housing is going lower and pay Option ARMs will be the next crisis that will send the credit markets stumbling. You can bank on that.

***

Comment by Scott

June 14th, 2008 at 1:28 pm

While WAMU, WB and CFC maybe in a class of their own with option ARM loans the worrying thing is that other sizable banks with no major exposure to these loans or California are also in trouble. Banks that operate in the Southeast like SunTrust or the South, like Regions are tanking. OK Florida isn’t doing well but these and other banks are hurting because of construction loans as much as their retail loans.

Need I say that Lehmans was the investment banker that handled Wachovia’s acquisition of Golden West and is now tanking because of its own portfolio of unknowns. Those banks like National City, Citi and Wamu that have been raising capital either under the orders or requests of banking regulators have done so and burned their new investors in the process. WAMU sold shares for $8.50 when the market prices was $10-11 but did the investors get a deal? NO! They are underwater now too with WAMU at $6.50. Ditto for CITI and National City which has fallen below the $5 danger threshold.

Yet these and other banks still need to raise capital. From where will it come? If the pioneers in the recapitalization process have seen their investments sour within months of their investing billions who is going to follow especially as the drumbeat of writedowns shows no sign of abating. Without fresh capital banks have to shrink their lending levels down to what their remaining capital can support. The Fed can temporize by exchanging its assets for bank debt but bad debt doesn’t go away in this process and the Fed, so far, has insisted it be made whole if the debt it takes as collateral goes south.

At the other end of the credit bubble are the GSE’s who are taking on the vast majority of new mortgage lending made possible by the FED’s largesse. So, at either end of the credit bubble we are being backstopped by quasi governmental institutions assuming the credit risks of a banking industry no longer sufficiently capitalized to this itself.

The bubble bursts when the first of these quangoes goes to the Congress for an appropriation to cover losses it has sustained propping the banking system up. I don’t see any other way out and given the stress on the consumer and business by rising ‘non core inflation’, aka as the ‘real world’, can there be any doubt that either the FED or the GSEs are going to be taking some serious hits by holding or underwrting all this private debt.

By Dr. Housing Bubble

June 14th, 2008

Source

The next stage of the mortgage debacle is only starting to rear its ugly head and all early signs tell us that this is going to be even worse than the subprime mortgage collapse. We need to remember that the subprime mortgage debacle was only one facet of a global debt boom that has taken a stranglehold over the industrialized world. The United Kingdom is now starting to realize that even they are going to face a housing meltdown. Yet there is still a perception out there from pundits and those in the media that this housing meltdown was caused purely by subprime loans, which could not be anything further from the truth.

Many understand that this is a debt bubble and not only a collapse fueled by the subprime market in which low-income people bought overpriced homes. That in fact is a big player in this mess but many who once thought they were “prime” are going to be realizing there is nothing prime about them. Welcome to the even uglier side of things which is only in stage one at the moment. We now enter the Pay Option ARM debacle:

The most ominous sign of the above chart is the following:

-$500 Billion in total Pay Option ARMs outstanding in the U.S.

-60 Percent of these issued to folks in California

The Pay Option ARM is one of the most poorly construed mortgage product ever to face this planet. It was a pathetic attempt to allow a larger majority of Americans to have a piece of the great American credit ponzi scheme. Many of these loans give you the following pay options on a mortgage:

-Fully Amortizing 30-year payment - you pay both principal and interest on a 30-year schedule

-Fully Amortizing 15-Year Payment - you pay both principal and interest on a 15-year schedule

-Interest-Only payment - covers only the interest portion of the mortgage and does not pay down principal

-Minimum Payment - the most widely picked option in which your payment is set for 12 months at an introductory rate (remember those absurd intro rates?). After that, payment changes are made annually and a payment cap limits how much it can increase or decrease each year.

Just to show you how financially destructive these mortgage products will be let us look at a $500,000 loan with a teaser 1.25% intro rate:

*Source: http://mortgage-x.com

The loan if it were to be paid in 30-years carries a $3,010 monthly principal and interest payment while the intro teaser rate only required the owner to pay $1,666 per month deferring a large amount of the payment to a later date. You may be wondering, “well I’m sure only a handful of people opted to pay the minimum payment right?” Wrong.

“(Businessweek 2006) Now the signs of excess are crystal clear. Up to 80% of all option ARM borrowers make only the minimum payment each month, according to Fitch Ratings. The rest of the money gets added to the balance of the mortgage, a situation known as negative amortization. And once balances grow to a certain amount, the loans automatically reset at far higher payments. Most of these borrowers aren’t paying down their loans; they’re underpaying them up.

Yet the banking system has insulated itself reasonably well from the thousands of personal catastrophes to come. For one thing, banks can sell some of their option ARMs off to Wall Street, where they’re packaged with other, better loans and re-sold in chunks to investors. Some $182 billion of the option ARMs written in 2004 and 2005 and an additional $83 billion this year have been sold, repackaged, rated by debt-rating agencies, and marketed to investors as mortgage-backed securities, says Bear, Stearns & Co. (BSC )Banks also sell an unknown amount of them directly to hedge funds and other big investors with appetites for risk.

The rest of the option ARMs remain on lenders’ books, where for now they’re generating huge phantom profits for some lenders. That’s because, according to generally accepted accounting principles, or GAAP, banks can count as revenue the highest amount of an option ARM payment — the so-called fully amortized amount — even when borrowers make only the minimum payment. In other words, banks can claim future revenue now, inflating earnings per share.”

And for those of you who say we didn’t see this coming, that paragraph was pulled from a Businessweek article in 2006 title “nightmare mortgages.” Of course, Wall Street is no longer buying this crap so that $500 billion is going to implode and no one is going to stop it. Also, you need to remember that 60 percent of that mortgage portfolio of Pay Option ARMs is here in sunny California making us confront a $300 billion time bomb.

80% only made the minimum payment on these toxic waste products. I’ll draw your attention once again to that new chart recently released by Businessweek. What you’ll notice is that the gray bars are a better indicator of how quickly we will face this implosion since only a small minority were actually paying either the interest only or the 30-year options. California as a state is now down 30 percent in one-year and many niche markets are going to face 40 or even 50 percent drops. This will prove to be a bigger hit on the California housing market as we will see in the upcoming months.

Many of these mortgages now have larger balances! That is the absurdity of these mortgage products. If you really think about it, the minimum payment will actually increase the underlying amount you owe almost assuming your home will appreciate in the Wonderland reality of many homeowners and lenders. Now we have a somewhat cruel fate in which California median prices are crashing while many of these option ARM products have been slowly growing in the past few years. That is why lenders such as WaMu, Wachovia, and Countrywide who specialized in these toxic waste products are down by:

WM: down 84% from 6/14/2007

CFC: down 87% from 6/14/2007

WB: down 65% from 6/14/2007

Why do you think these companies are down so much? Aside from the subprime collapse they have seen nothing in regards to the option ARM debacle that is squarely facing them. $300 billion in mortgages alone in California that are worth so much less! Let us assume that these products are now only worth half of that $300 billion. That means California alone, not even counting the other $200 billion out there is going to hurt many direct lenders or Wall Street firms via writedowns by $150 billion with an almost guarantee given the 30 percent market decline. Let us do a quick market cap calculation of these 3 sample companies:

Marketcap as of 6/14/2008:

WM: $7.02 billion

CFC: $2.82 billion

WB: $38.89 billion

Total: $48.73 billion

Bwahaha! There combined marketcap is only about a third of the losses of pay Option ARMs which one state (California) will be facing! What if we factor that other $200 billion which undoubtedly will be facing losses as well given the nationwide scope of this housing debacle? Of course there are other lenders out there who dished out these toxic products but the above 3 were major players. Now you know why these institutions are off by ridiculous amounts. If you simply do the basic accounting and take the pulse of the market, you know that this has the potential of flooding lenders with a stream of losses for a few more years or until they go under. Take a look at the distress numbers for California last month:

May 2008:

NODs: 41,965

NTS: 9,728

REOs: 20,237

Total for California: 71,930

Nationwide total: 261,255

California makes up 27.5% of all foreclosure filings in May of 2008. Just to give you an idea how bad things are getting in California let us look at the stats for May of 2006:

May 2006:

NODs: 7,794

NTS: 804

REOs: 138

Total for California: 8,736

Nationwide total: 92,746

*Source: Realtytrac

So only two years ago, California made up 9.4% of all nationwide foreclosure filings and now we stand at 27.5%. This is how quickly things are coming apart at the seams and we haven’t even seen the first peak of option ARM recasts which should occur in October through December of this year. If you don’t think that $500 billion is a lot just wait until this summer selling season falls flat on its face for California. Fall and winter are going to be brutal.

Many of these owners are going to be highly tempted to moonwalk away from their mortgages. Does Bank of American really want to assume this option ARM time bomb? They are scheduled to close their deal with Countrywide sometime in the third quarter yet I simply do not see how they avoid astronomical losses on the current mortgage portfolios and REO properties. Unless California suddenly goes into another bubble and prices start going up, we are in for a tough few years and the current California multi-billion dollar budget short fall isn’t pretty either. Keep in mind the California budget which has now been revised to a $17 billion short fall is going to force us to make some hard decisions. Either raise taxes to plug budget gaps or cut spending (aka jobs) and only increase the unemployment numbers and thus depress the economy further.

No matter how you slice it, California housing is going lower and pay Option ARMs will be the next crisis that will send the credit markets stumbling. You can bank on that.

***

Comment by Scott

June 14th, 2008 at 1:28 pm

While WAMU, WB and CFC maybe in a class of their own with option ARM loans the worrying thing is that other sizable banks with no major exposure to these loans or California are also in trouble. Banks that operate in the Southeast like SunTrust or the South, like Regions are tanking. OK Florida isn’t doing well but these and other banks are hurting because of construction loans as much as their retail loans.

Need I say that Lehmans was the investment banker that handled Wachovia’s acquisition of Golden West and is now tanking because of its own portfolio of unknowns. Those banks like National City, Citi and Wamu that have been raising capital either under the orders or requests of banking regulators have done so and burned their new investors in the process. WAMU sold shares for $8.50 when the market prices was $10-11 but did the investors get a deal? NO! They are underwater now too with WAMU at $6.50. Ditto for CITI and National City which has fallen below the $5 danger threshold.

Yet these and other banks still need to raise capital. From where will it come? If the pioneers in the recapitalization process have seen their investments sour within months of their investing billions who is going to follow especially as the drumbeat of writedowns shows no sign of abating. Without fresh capital banks have to shrink their lending levels down to what their remaining capital can support. The Fed can temporize by exchanging its assets for bank debt but bad debt doesn’t go away in this process and the Fed, so far, has insisted it be made whole if the debt it takes as collateral goes south.

At the other end of the credit bubble are the GSE’s who are taking on the vast majority of new mortgage lending made possible by the FED’s largesse. So, at either end of the credit bubble we are being backstopped by quasi governmental institutions assuming the credit risks of a banking industry no longer sufficiently capitalized to this itself.

The bubble bursts when the first of these quangoes goes to the Congress for an appropriation to cover losses it has sustained propping the banking system up. I don’t see any other way out and given the stress on the consumer and business by rising ‘non core inflation’, aka as the ‘real world’, can there be any doubt that either the FED or the GSEs are going to be taking some serious hits by holding or underwrting all this private debt.