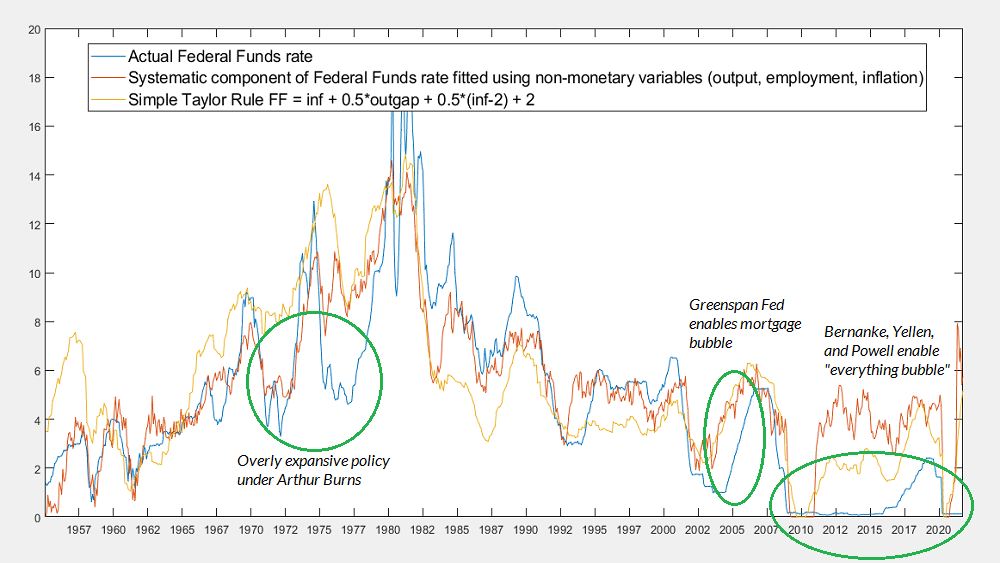

'..we enter 2022 amid the most extreme financial bubble in U.S. history, driven by yield-seeking speculation, amplified by a Federal Reserve that has abandoned any tether to systematic monetary policy .. The “policy error” [see image] of the Fed is already behind us, and can be measured by the gap between what the Fed has actually done, and what any reasonable basket of systematic policy guidelines would have suggested instead.''In an economy where the Fed has lost every systematic tether to common sense, empirical evidence, and concern for financial stability, it’s worth beginning this first market comment of 2022 by recalling the ways we’ve adapted in order to navigate that environment. In a world where securities are regularly described on CNBC as “plays,” it’s clear is that the financial markets presently have little to do with “investment” – at least not by Benjamin Graham’s definition as “an operation that, upon thorough analysis, promises safety of principal and an adequate return.”

It may be true that zero interest rates provide investors “no alternative” but to speculate. But as Graham emphasized, there are many ways in which speculation can be unintelligent. The first of these is speculating when you think you are investing.

..

Until the catastrophic consequences of Fed-induced speculation become unavoidable, the reality is that all we can do is deal with it..

..

..how deranged Federal Reserve policy has become. I use that word advisedly: deranged as in wildly outside of historical bounds, and also deranged as in intellectually unsound. The most important issue facing the Fed here isn’t how quickly to taper its asset purchases, or when the next rate hike should occur. The real problem for the Fed is that it has completely abandoned any semblance to a systematic policy framework, in apparent preference for a purely discretionary one.

Systematic policy means that your policy variables are correlated with, and informed by, current, lagged, and projected data on output, employment, and inflation. There are numerous systematic policy benchmarks, or a basket of them, that could be used – even as very loose guidelines – to tether Fed policy decisions to observable data. It’s easy to estimate whether deviations from systematic policy benchmarks have a large effect on subsequent economic activity (the answer is that they do not). Instead, the modern Federal Reserve has committed itself to operating monetary policy entirely by the seat of its pants.

A systematic policy would allow individuals and financial markets to anticipate the general stance of monetary policy based on observable data. Instead, the Federal Reserve has fashioned itself into a reckless circus clown handing out lollipops to diabetic toddlers. Having taught them that they will be continually appeased, regardless of the long-term consequences, even a “taper” is now met with wails of surprise, crisis, and tantrum.

The Federal Funds rate remains pegged at zero, with the monetary base at nearly 28% of GDP. This, despite 7% CPI inflation, 3.9% unemployment, real output just 1.6% shy of the CBO estimate for potential GDP, and yield-seeking financial speculation that has driven the equity market to the highest valuations and lowest yields of any point in U.S. history outside of the 2000 market peak.

The current level of the monetary base relative to GDP is utterly at odds with Section 2A of the Federal Reserve Act, which instructs the Fed to “maintain long-run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production.” The ratio of base money to GDP never exceeded 16% before 2008. The nearest alternative to holding zero-interest base money is to hold a Treasury bill, and 16% of GDP in zero interest base money is already sufficient to drive T-bill rates to zero. Until the Federal Reserve contracts its balance sheet by half, the only way the Fed can raise short term interest rates above zero is by explicitly paying interest to banks on their excess reserves (IOER).

..

Taken together, we enter 2022 amid the most extreme financial bubble in U.S. history, driven by yield-seeking speculation, amplified by a Federal Reserve that has abandoned any tether to systematic monetary policy. Across history, with few exceptions – and none that worked out well – policy tools like the Fed Funds rate and the ratio of base money to GDP have typically had a reasonably strong correlation with observable economic data – unemployment, inflation, and the GDP output gap. The “policy error” [see

image] of the Fed is already behind us, and can be measured by the gap between what the Fed has actually done, and what any reasonable basket of systematic policy guidelines would have suggested instead.'

- John P. Hussman, Ph.D.,

Return-Free Risk, January 14, 2022

Context'..the thought-provoking assessment of Wolfgang Münchau in his Eurointelligence column Let's talk Ponzi.'

-

Fed Operations Look More Like a Ponzi Scheme Than Bitcoin or Ethereum, January 10, 2022

Astrologers Would Likely Beat the Fed at Inflation Forecasting, January 14, 2022

(An economic Ponzi scheme) – Evergrande Moment – ‘China Evergrande is not ‘too big to fail’, says Global Times editor’(Banking Reform) - Issues 2022 - 'Our nation (and the world) was profoundly scarred by the Great Depression experience..'(Banking Reform - English/Dutch) '..a truly stable financial and monetary system for the twenty-first century..' {kind=link}