'Until specialists and society in general fully grasp the essential theoretical and legal principles associated with money, bank credit, and economic cycles, we may realistically expect further suffering in the world due to damaging economic recessions..'

- Dr. Jesús Huerta de Soto,

Banking Reform - English/Dutch) '..a truly stable financial and monetary system for the twenty-first century..''..As Niall Ferguson, Charlie Calomiris, and others have pointed out, governments regulate and structure banking systems first and foremost to facilitate government finance, not private capital markets.'

- Streetwise Professor (

Source, March 19, 2023)

'..fractional banking implodes. Which is what happened in 1997 and 2007 — and what I saw unfold in the sushi restaurant last month .. ..The dangerous weakness of fractional banking is that if nobody has a reason to panic, banks are safe; but if everyone runs, a bank can collapse, even if it previously passed tests on issues such as capital adequacy..''In some senses, it felt wearily familiar. I have watched two financial crises unfold before: once in 1997 and 1998 in Tokyo, as an FT correspondent, when Japanese banks imploded after the 1980s bubble; then in 2007 and 2008, when I was capital markets editor in London during the global financial crisis. I wrote books on both.

Those events taught me a truth about finance that we often ignore. Even if banking appears to be about complex numbers, it rests on the slippery and all-too-human concept of “credit”, in the sense of the Latin credere, meaning “to trust” — and nowhere more than in relation to the “fractional banking” concept .. The fractional banking idea posits that banks need to retain only a small proportion of the deposits they collect from customers, since depositors will very rarely try to get all their money back at the same time. That works brilliantly well in normal conditions, recycling funds into growth-boosting loans and bonds. But should anything prompt depositors to grab their money en masse, fractional banking implodes. Which is what happened in 1997 and 2007 — and what I saw unfold in the sushi restaurant last month.

..

..items considered “safe” can be particularly dangerous because they seem easy to ignore. In the late 1990s, Japanese bankers told me that they made property loans because this seemed “safer” than corporate loans, because house prices always went up. Similarly, bankers at UBS, Citi and Merrill Lynch told me in 2008 that one reason why the dangers around repackaged subprime mortgage loans were ignored was that these instruments had supposedly safe triple-A credit ratings — so risk managers paid scant attention.

So, too, with SVB: its Achilles heel was its portfolio of long-term Treasury bonds that are supposed to be the safest asset of all; so much so that regulators have encouraged (if not forced) banks to buy them. Or as Jamie Dimon, head of JPMorgan, noted in his annual shareholders’ letter, “ironically banks were incented to own very safe government securities because they were considered highly liquid by regulators and carried very low capital requirements”. Rules to fix the last crisis — and create “safety” — sometimes create new risks.

..

..The dangerous weakness of fractional banking is that if nobody has a reason to panic, banks are safe; but if everyone runs, a bank can collapse, even if it previously passed tests on issues such as capital adequacy — unless a government steps in. And while the government never used to worry about smaller banks collapsing, now they fear the digital domino effect.

..

..I also fear that the past decade of quantitative easing has distorted finance so deeply that there will be unexpected chain reactions, if not in banks, then other corners of finance.

SVB might now have a place in the history books. Sadly, this story is unlikely to end here.'

- Gillian Tett,

What I learnt from three banking crises, April 6, 2023

'Some years back, I dedicated a weekly CBB to the tedious process of walking through a series of debit and Credit accounting entries to illuminate how a GSE would issue short-term debt obligations (IOUs) to a money market fund and use this liquidity to purchase securities from an investment firm or hedge fund – where this liquidity would circulate through the system until being redeposited into the money market. The GSE would then tap this liquidity to issue additional IOUs to purchase more securities – and this process could basically repeat indefinitely. It was fractional reserve banking with the old “deposit multiplier” – a dynamic throughout history responsible for devastating Credit booms and busts. There was, however, one momentous difference: Not subject to bank reserve requirements, GSE borrowing and lending operations were unfettered - with powerful and far-reaching “infinite multiplier” effects.''The CBB has a 25-year history of chronicling GSE developments. I have a long-held view that the GSEs – with their implicit government guarantees and far-flung missions – are dangerous financial institutions that have played an instrumental role in the multi-decade Credit Bubble.

I began closely monitoring the GSEs in 1994, after recognizing they were operating as quasi-central banks. Their aggressive securities purchases provided a critical liquidity backstop during a period of intense hedge fund bond market deleveraging (sparked by Fed tightening after an extended period of extraordinarily depressed policy rates). GSE (chiefly Fannie and Freddie) assets expanded an unprecedented $151 billion in 1994, to $782 billion. The 1998 Russia/LTCM collapses induced record one-year GSE growth of $353 billion, to $1.622 TN (as of Q3 ’99). Hamstrung by Fannie and Freddie accounting scandals, one-year GSE growth nonetheless reached a new peak of $418 billion, to $3.360 TN (as of Q2 ’08), during the instability leading up to the 2008 crisis.

GSE growth last year reached an unprecedented $921 billion, to a record $9.224 TN – with three-year growth of $2.094 TN, or 29.4%. And it would not be surprising to see FHLB/GSE Q1 growth well in excess of $500 billion. Over the years, I’ve tried to explain how Washington guarantees (explicit and implicit) and resulting market distortions create unlimited capacity for the GSEs to borrow and extend Credit. Especially during crisis environments, the GSEs readily issue shorter-term debt instruments – including debt securities purchased by the money market fund complex.

Some years back, I dedicated a weekly CBB to the tedious process of walking through a series of debit and Credit accounting entries to illuminate how a GSE would issue short-term debt obligations (IOUs) to a money market fund and use this liquidity to purchase securities from an investment firm or hedge fund – where these funds would circulate through the system until being redeposited into the money market. The GSE would then tap this liquidity to issue additional IOUs to purchase more securities – and this process could basically repeat indefinitely. It was fractional reserve banking with the old “deposit multiplier” – a dynamic throughout history responsible for devastating Credit booms and busts. There was, however, one momentous difference: Not subject to bank reserve requirements, GSE borrowing and lending operations were unfettered - with powerful and far-reaching “infinite multiplier” effects.

I appreciate that this pithy explanation is likely not overly satisfying. But this “infinite multiplier” – especially in crisis environments – affords the GSEs the capacity to essentially provide a central bank-style liquidity backstop. It is therefore reasonable to add the FHLB’s (at least) $304 billion to the Fed’s $391 billion – to calibrate the magnitude of system liquidity injections second only to Covid craziness. For perspective, Fed Credit expanded $605 billion over three weeks to accommodate deleveraging during the acute phase of the October 2008 market crisis.

The Powell Fed today confronts a historic dilemma. And it is uncomfortably reminiscent of how Federal Reserve officials faced in 1929 a confluence of a weakening economy, a fragile banking system, and a crazy stock market speculative Bubble. Ben Bernanke is fond of pointing blame for the crash and subsequent banking crisis to the “Bubble poppers”. More grounded analysis would recognize that Bubbles do inevitably burst, and the greater the inflation – the more protracted the “Terminal Phase” of excess – the more vulnerable the financial system and economy are to collapse.

Importantly, each bailout and reflation ensures only larger Bubbles – greater amounts of debt, financial system leverage, and speculative excess. The Fed’s $1 TN 2008 QE inflated to massive $5 TN pandemic reflationary measures. It’s distressing to contemplate how much the Federal Reserve’s balance sheet will inflate to accommodate the next serious de-risking/deleveraging crisis. And while most will scoff today at the notion of a systemic “fire”, the reality is that the system suffered bank failures and a run on deposits, with unemployment at 3.6% and Q1 GDP growth expected at about 2.5% (Atlanta Fed GDPNow forecast). The massive liquidity response only exacerbates perilous market instability.

- Doug Noland,

That Was Interesting, March 31, 2023

'..As this “everything bubble” unwinds .. Since 2008, the Fed has become so comfortable with loose collateral requirements (including treating unsecured junk bonds as their own collateral) that Ponzi finance has apparently become standard operating procedure.''The simplest thing that can be said about current financial market and banking conditions is this: the unwinding of this Fed-induced, yield-seeking speculative bubble is proceeding as one would expect, and it’s not over by a longshot.

I expect that FDIC-insured, and even most uninsured bank deposits will be fine. I also expect that hedged investments will be fine. In contrast, a great deal of market capitalization that passive investors count as “wealth” will likely evaporate, possibly including steep losses to bank shareholders and unsecured bondholders. Investors and policy-makers have confused speculation and extreme valuations with “wealth creation,” but it never was. A parade of seemingly independent “crises” will emerge as this bubble unwinds, including bank failures, pension strains, and market collapses, but they all have the same origin .. As explained in more detail at the end of this comment, I continue to expect a loss on the order of -58% in the S&P 500, from current levels, over the completion of this cycle. Nothing in our investment discipline relies on that outcome, but having correctly anticipated the extent of the 2000-2002 and 2007-2009 collapses, it’s best not to rule it out.

..

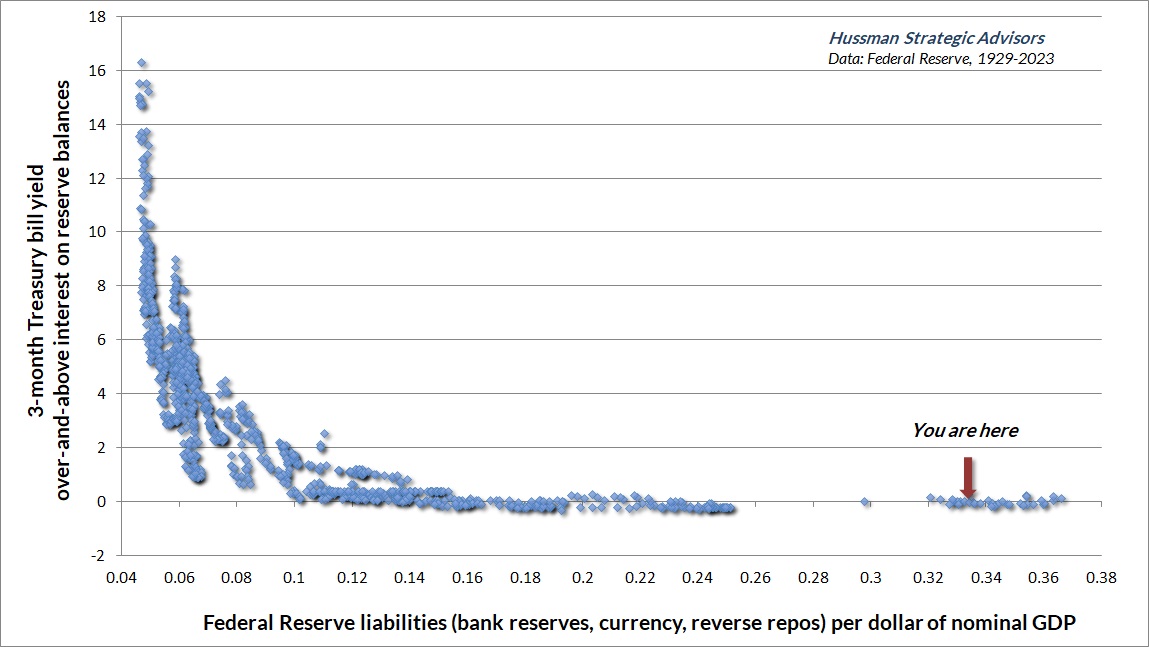

The

chart below requires no statistics or curve-fitting. Just a dot for every month since 1929. It presents monetary policy in a nutshell. By early-2022, the Fed was forcing the public to choke down a breathtaking 36% of GDP in zero-interest money, passing like stale, re-gifted fruit cakes from one holder to another (how’s that one Dave?), fueling yield-seeking speculation in every security that might offer the hope of something more than “zero.”

Then the prices of those securities fell. One can blame inflation, and imagine that the Federal Reserve’s interest rate hikes “caused” the crisis. But the fact is that crisis has been baked into those stale, re-gifted fruit cakes for years. Avoiding a crisis required speculative valuations and record-low interest rates to be sustained forever.

As I’ve noted during previous bubbles, a market collapse is nothing but risk-aversion meeting an inadequate risk-premium; rising yield pressure meeting an inadequate yield. The extreme valuations encouraged by years of deranged Fed policy are unwinding, and based on the gap between prevailing investment valuations and even modest historical norms, it’s not over by a longshot.

Lessons from the global financial crisisExcerpted from the section titled “Diary of a deranged ‘ample reserves regime” in the September 2022 comment,

Now Comes the Hard PartRecall how we got a mortgage bubble in the first place. Following the 2000-2002 market collapse, Alan Greenspan cut short-term interest rates to just 1%, driving investors to search for alternatives that might offer a higher return. They found that alternative in mortgage securities, which provided a “pickup” in yield over and above T-bills, as well as perceived safety, given that U.S. housing prices had never collapsed.

With demand for mortgage securities driven by yield-seeking speculation, and supply driven by Wall Street’s eagerness to sell new “product,” the result was an explosion in the volume of mortgage securities. But in order to create a mortgage security, you have to make a mortgage loan. Enter no-doc mortgages, zero-down interest-only payment structures, and a resulting bubble in housing prices. Then came the hard part. The Fed did not save the economy from the global financial crisis. The Fed caused it.

Indeed, the thing that finally ended the global financial crisis wasn’t Fed heroism, distressed asset purchases, or quantitative easing. It was a change in accounting rule

FAS-157 by the Financial Accounting Standards Board in March 2009, which eased “mark to market” standards for banks, eliminating the prospect of widespread bank insolvency by making insolvency opaque. The decade of zero interest rates that followed simply helped banks to recapitalize their balance sheets, funded by paying depositors zero.

The same dynamic that created the mortgage bubble – yield-seeking speculation driven by a pile of zero interest monetary hot-potatoes – is precisely what has now given us the broadest speculative episode in U.S. history. The speculation has been broader and more sustained because the Federal Reserve’s profligacy has been greater .. The rampage won’t end until the Fed reins in the Bernankenstein Monster it unleashed more than a decade ago.

..As this “everything bubble” unwinds, it may be impossible to deal with the mess the Fed has created without protecting more depositors than the FDIC would normally cover, and without taking receivership of more banks than Wall Street would prefer.

..

One is reminded that a key feature of Ponzi schemes is that withdrawals by early investors are financed with other people’s money, rather than by sound assets. They work only because the accounting is fraudulent, so nobody realizes that the scheme is insolvent. Since 2008, the Fed has become so comfortable with loose collateral requirements (including treating unsecured junk bonds as their own collateral) that Ponzi finance has apparently become standard operating procedure.

Nobody even blinks that Janet Yellen earned $7.2 million in “speaking fees” from major banks and corporations in the interim between serving as Fed Chair and Treasury Secretary. Come on now. I don’t want to be mean, but have you ever heard Janet Yellen speak?

..

The Federal Reserve’s “ample reserves regime” has not only encouraged the most extreme speculative bubble in history, it has created a host of other distortions that now include bank failures. The faster the Fed can wind down its balance sheet the better. Zero-interest reserves can certainly amplify speculation, but they’re not magic beans. Indeed, since the Fed launched quantitative easing in 2008, commercial bank loans (total commercial, industrial, consumer, and real-estate) have grown at an average annual growth rate of just 3.6% – the

slowest rate of any point during the post-war era, and a fraction of the 9.3% pre-QE average.

As I’ve detailed

previously, there’s no compelling evidence that the trajectory of GDP or employment in response to activist Federal Reserve interventions has been any different than one could have projected using non-monetary variables alone. If extraordinary monetary policy matters, information about monetary variables should improve our ability to explain subsequent movements in real GDP and employment. If it doesn’t, the forecasts will be largely the same with or without the monetary information. That’s exactly what we observe.

When interest rates are zero, a massive balance sheet drives speculation..

..

As for the Federal Reserve’s immediate dilemma – whether to continue to raise interest rates to fight inflation, or put a hold on further rate hikes – a few observations from my December comment,

They’ve Ruled Out Tail Risk may be useful:

“On the subject of interest rates and inflation, I’ll reiterate that the single best predictor of year-ahead inflation is current year-over-year inflation, and the second-best predictor is last year’s inflation rate .. What’s striking, though, is how little impact interest rate hikes themselves have in reducing inflation, except in economic environments that involve fear and risk-aversion – recession or banking crises. While rate hikes do tend to weaken housing, durable goods, and capital investment, the impact is typically not enough to reverse an inflationary trend.

..

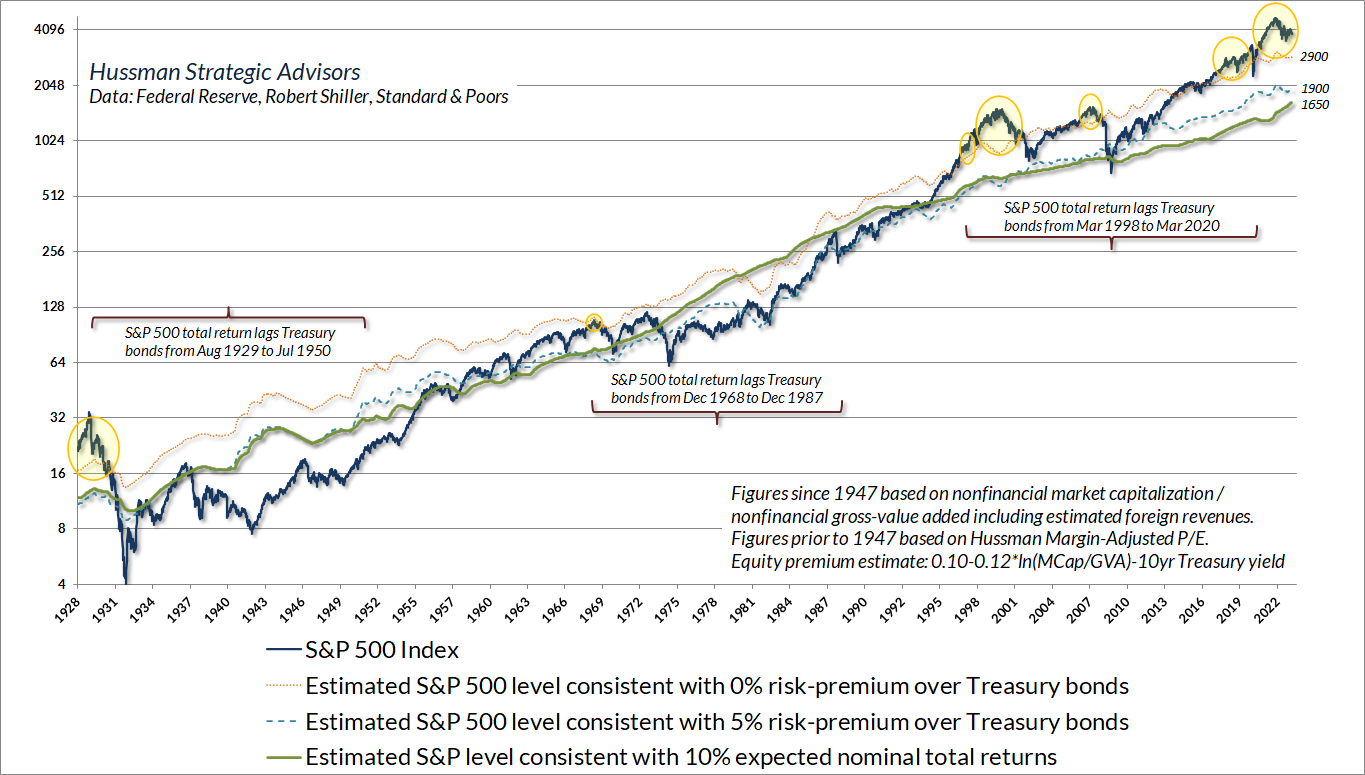

With regard to current financial market conditions, several updated charts will help to explain why we continue to estimate the potential for severe downside market risk. The green line in the

chart below shows the level of the S&P 500 that we associate with run-of-the-mill expected returns averaging 10% annually. The blue dotted line is the level we associate with a historically run-of-the-mill 5% premium over-and-above Treasury yields, and the orange dotted line shows the level of the S&P 500 that we associate with 10-year expected returns no better than those of 10-year Treasury bonds. The yellow bubbles show periods when our 10-year estimate for S&P 500 total returns was below the prevailing 10-year Treasury bond yield.

..

Since ragged, divergent internals are typically an indication of risk-aversion among investors, we view the combination of extreme valuations and poor market internals as a “trap door” situation. We continue to face that combination at present. If internals were to improve, we would suspend our bearish outlook even here, shifting to a neutral or constructive outlook, albeit with position limits and safety nets. For now, market conditions are not only unfavorable but increasingly fragile..'

- John P. Hussman, Ph.D.,

Edge of the Edge, March 19, 2023

Context '..a process of transition toward the only world financial order..' - Jesús Huerta de Soto(Banking Reform) - 'Financial regulators have ignored their post-2008 rule book to contain the latest banking panic.'

'..a “monstrous” (according to Clemente de Diego) legal institution..'Fed Policy: It's Not Fractional Reserve Banking, It's ZERO Reserve Banking, March 21, 2023

'The "Manic-Depressive" Economy .. spirit becomes corrupted .. are of high human and personal cost..'(Banking Reform)(Ethics) - 'A stable financial system .. [doesn't] exist in the U.S.' - The Wall Street Journal Editorial Board(Banking Reform) - 'Disaster is a strong but appropriate word that applies perfectly to the state of U.S. monetary policy..' - Dr. Hunt'U.S. inflation is currently 6.8%, the highest rate in the developed world .. Almost universally, rates have been kept lower than the Taylor Rule had suggested..', 2021

Ethical Affective Ambiance in the Electric Universe – Production of Money, Prices and Market{kind=link}

{kind=link}